Introduction

Healthcare is deep into a cloud-first decade, where digital transformation, data-driven decision-making, and scalable cloud platforms are reshaping how care is delivered and managed. Electronic health records, imaging, telehealth, remote patient monitoring, and AI-driven diagnostics now depend on infrastructure that can expand quickly, connect ecosystems, and keep protected health information secure.

As more hospitals and payers modernize their technology stack, digital transformation in healthcare is accelerating the shift toward cloud-native platforms that support interoperability, scalability, and real-time data access. As a result, the healthcare cloud computing market is becoming a central layer of digital health rather than a side project.

This overview walks through current market size, adoption and usage patterns, segmentation, regional dynamics, key trends, real-world use cases, and future growth opportunities so teams can plan investments with data instead of instinct.

What Is Healthcare Cloud Computing

Healthcare cloud computing refers to the delivery of computing resources such as storage, servers, databases, analytics, and applications over the internet to support clinical and non-clinical workflows. Instead of hosting systems in local data centers, healthcare organizations subscribe to public, private, or hybrid cloud services that scale on demand while meeting strict privacy and compliance requirements.

In practice, this includes cloud-based EHR platforms, PACS and medical imaging archives, population health and claims analytics, patient engagement portals, telehealth platforms, and data integration layers that connect hospitals, clinics, payers, and device ecosystems. Cloud architecture helps providers and payers improve interoperability, reduce infrastructure overhead, and respond faster to new care models and regulatory change.

Healthcare Cloud Computing Market Overview

A Rapidly Expanding Core Layer of Digital Health

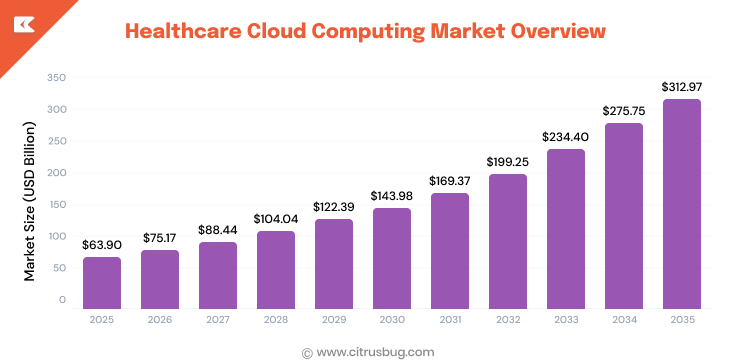

The global healthcare cloud computing market is moving from early digitization to large scale modernization. By 2025, the market is valued at about USD 63.9 billion, reflecting the cumulative impact of EHR rollouts, imaging consolidation, and basic data hosting. Within a year, this value reached roughly USD 75.17 billion in 2026 as more workloads shift from on-premises infrastructure to managed cloud environments.

Longer term, the sector is expected to expand at an annual rate of around 17.22%, indicating that cloud services are not a niche line item but one of the strongest growth engines in healthcare technology. That rate reflects vendor investment in specialized healthcare cloud platforms, increasing demands for real time analytics, and the scaling of AI models that require elastic computing capacity.

Broad Industry Adoption

Adoption is already broad across the industry. Around 85% of healthcare organizations use some form of cloud computing technology, which means decisions are less about whether to use cloud and more about which workloads to prioritize and how to optimize architectures. Approximately 50% of organizations report using hybrid cloud setups that combine public and private environments, showing how risk-sensitive health systems balance performance, control, and compliance.

Taken together, these statistics highlight a healthcare cloud market that already holds significant revenue, grows at double-digit rates, and has widespread adoption as a foundation for digital care delivery.

Adoption And Usage Statistics In Healthcare Cloud Computing

Remote Monitoring and Device-Driven Data Flows

- In the United States, wearable medical devices have become a mainstream source of health data, with about 30% of Americans using such devices in 2024. These wearables feed large volumes of continuous information into cloud-based monitoring and analytics platforms, which in turn support early intervention and chronic disease management.

- Remote patient monitoring programs that depend on cloud infrastructure are scaling quickly. The number of remote patient monitoring users in the United States reached approximately 68.3 million in 2024 and is expected to rise to about 84.6 million in 2025, supported by reimbursement coverage and provider demand for home-based care models.

Service-heavy Adoption Models

- Service-centric deployments dominate many cloud projects. Service offerings account for around 82% of the market in 2024, reflecting reliance on managed services, implementation, integration, and ongoing support rather than just raw infrastructure.

- Healthcare provider organizations represent the bulk of end-use activity in this segment, with provider end-use capturing roughly 70% share in 2024. This indicates that hospitals, clinics, and health systems drive most of the cloud workload volume, while payers and other stakeholders account for a smaller but still meaningful slice.

These adoption patterns show how the healthcare cloud computing market is intertwined with connected devices, remote monitoring programs, and service-heavy operating models that reduce the need for in-house infrastructure management.

Segmentation Insights In The Healthcare Cloud Computing Market

Cloud Deployment Patterns

Within the healthcare cloud market, deployment choice shapes how organizations balance flexibility, control, and regulatory posture. Public cloud environments capture a significant share, representing about 54.72% of the market in 2026. This reflects growing confidence in public cloud security controls, dedicated healthcare offerings, and the scalability required for analytics and AI workloads.

At the same time, many health systems maintain private or institution-specific environments for sensitive data and high-control workloads. Private deployments secure a substantial portion of market share in parallel with public platforms, and hybrid models are common in practice even when contracts are categorized under one deployment label. These patterns align with the earlier statistic that roughly half of organizations operate hybrid configurations, blending public cloud elasticity with private cloud governance.

Service Models and Clinical Application Focus

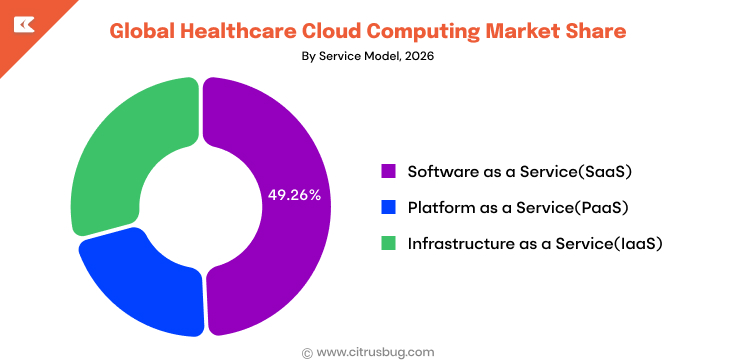

On the service model side, Software as a Service (SaaS) leads most implementations. SaaS captures close to 49.46% of the market in 2026, as hospitals and payers increasingly subscribe to cloud-hosted applications rather than installing monolithic software on local servers. This includes EHR modules, patient portals, scheduling and billing systems, and a wide range of speciality applications.

Clinical information systems account for a dominant share among application categories. Clinical information system workloads, such as EHRs, imaging viewers, and clinical decision support tools, make up around 62.06% of the market in 2026. This confirms that clinical care delivery remains the primary driver of cloud investment, with non-clinical applications such as finance, HR, and administrative systems following behind but gradually catching up through modernization waves.

End-user Landscape and Infrastructure Mix

End-user segmentation shows that financing entities and insurance organizations are also critical customers. Healthcare payers hold about 58.05% share within specific end user segments in 2026, reflecting their heavy reliance on cloud-based claims processing, fraud detection, and population health analytics. This reinforces that although providers generate much of the clinical data, payers help fund and scale the analytics infrastructure that runs on top of it.

Underneath these applications, cloud infrastructure components evolve as well. Hardware-oriented segments that supply compute, storage, and networking for healthcare clouds represent roughly 47.6% of the broader cloud infrastructure market in 2025. This mix highlights ongoing demand for high-performance infrastructure tuned for imaging, AI workloads, and large-scale data archival, even as service and software layers capture a greater share of visible value.

Overall, segmentation patterns show a healthcare cloud market led by public cloud deployments, SaaS delivery models, clinical information systems, and strong participation from both providers and payers on top of a sizable hardware and infrastructure base.

Regional Market Share And Growth Insights

North America

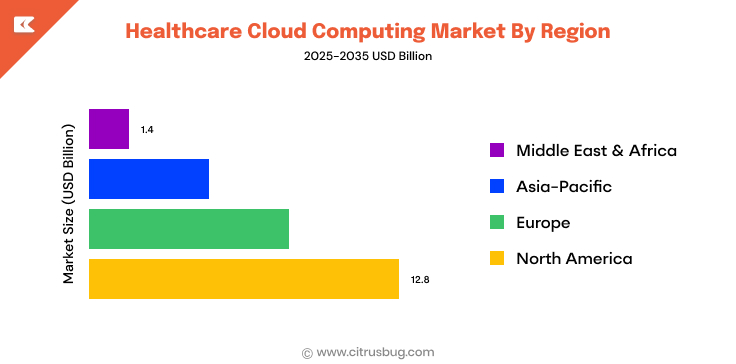

- North America holds the largest share of the healthcare cloud computing market, accounting for about 45% of global revenue in 2025. This dominance reflects mature EHR adoption, robust health IT regulation, and strong investment capacity among health systems and insurers.

Europe

- Europe represents approximately 30% of the market in 2025, driven by national level digitization programs, cross border data exchange initiatives, and ongoing modernization of hospital IT infrastructure across major economies such as Germany, France, and the United Kingdom.

Asia Pacific

- Asia Pacific captures around 20% of the healthcare cloud market trends in 2025 and is one of the most dynamic regions in terms of growth. The region is expected to expand at an annual rate of about 18.88% between 2026 and 2031 as countries scale universal health coverage, digital health platforms, and connected device ecosystems.

Middle East And Africa

- The Middle East and Africa region accounts for roughly 5% of global revenues in 2025. Although its current share is smaller, ongoing investments in national health information exchanges, smart hospital projects, and private healthcare expansion create room for sustained cloud adoption in the coming years.

These regional patterns indicate that while North America and Europe currently contribute the majority of revenue, Asia Pacific delivers some of the fastest growth rates, and emerging markets build a foundation for future expansion.

Key Trends Shaping Healthcare Cloud Computing

Shift From Infrastructure to Higher-Value Services

Healthcare organizations are moving beyond basic hosting to managed and value-added services. Non-clinical information systems, which include administrative and financial applications, are projected to grow at about 12.28% annually between 2026 and 2031. This indicates that finance, HR, and revenue cycle functions are steadily catching up with clinical systems in terms of cloud migration, simplifying operations for health systems that historically ran disparate on-premises tools.

Acceleration of Public Cloud as a Growth Engine

Public cloud platforms are expanding faster than many legacy deployment models. Revenue associated with public cloud in healthcare is expected to grow at roughly 18.30% per year from 2026 to 2031. This trend aligns with the increasing availability of healthcare-specific cloud services, enhanced data residency options, and compliance frameworks that satisfy stringent regulatory requirements while still providing elasticity and performance for analytics and AI workloads.

Hybrid Architectures and Advanced Infrastructure Layers

Hybrid cloud continues to play a strategic role as organizations distribute workloads across different environments. The hybrid cloud segment is projected to grow at close to 18% annually between 2024 and 2032, reflecting its role as a bridge between fully public and fully private models. In parallel, Infrastructure as a Service (IaaS) offerings that provide compute, storage, and networking as on-demand resources are expected to expand at around 19.4% per year over the same period, underpinning more sophisticated clinical and analytics applications.

Expanding Global Growth Baseline

Underpinning these segment-level trends is a strong overall growth baseline. The broader healthcare cloud and infrastructure space is anticipated to grow at a compound rate of approximately 16.71% from the mid 2020s onward, providing a supportive environment for vendors and health systems to plan multi-year investment roadmaps.

Collectively, these trends show a market that moves steadily away from isolated, on-premises systems toward integrated architectures that combine public, private, and hybrid cloud layers with increasingly sophisticated services.

Real World Use Cases Of Healthcare Cloud Platforms

Provider-Centric Transformation

- A significant majority of healthcare organizations are moving their systems to cloud-native platforms to streamline workflows and support digital care delivery. By 2025, an estimated 70% of healthcare organizations adopted industry cloud solutions, with 59% of providers already using them to enhance interoperability and service delivery.

- Cloud adoption helps providers to scale infrastructure and boost performance; for instance, 94% of health systems reported improved performance and availability after migrating to cloud solutions, enabling faster access to patient data and smoother operations across departments.

End-use Concentration among Providers

- Providers accounted for a significant majority of healthcare cloud adoption, with around 71.6% of total healthcare cloud market share attributed to providers in 2025, underscoring that hospitals and health systems remain the primary consumers of cloud platforms.

- Industry research consistently indicates that providers represent the largest share of cloud usage; for example, providers held 68.7% of the global health cloud market in 2024, driven by rising patient volumes and the growing need for scalable IT infrastructure.

These statistics reveal a market where practical use cases are anchored in provider organizations and service-heavy delivery models, with payers, life sciences companies, and other stakeholders layering on additional workloads across the same cloud ecosystems.

Future Outlook And Growth Opportunities

Rising Global Market Value Through Early 2030s

Forecasts suggest that the healthcare cloud computing market still has considerable headroom. Global revenues are expected to reach roughly USD 102.77 billion by 2031, reflecting continued migration of core clinical and administrative systems into cloud environments. As more health systems retire legacy data centers and consolidate applications, this trajectory positions cloud as the default hosting model for new digital health initiatives.

Another major forecast projects the global market value at around USD 189.51 billion by 2032. This level of spend indicates that cloud-based platforms will sit at the center of strategies for analytics, AI, precision medicine, and integrated care networks that cross organizational boundaries. It also suggests a growing role for specialized industry clouds that combine infrastructure, data, and applications in one stack.

Regional Growth Corridors

Regional forecasts highlight where future opportunities may be strongest. In North America, the healthcare cloud market is projected to reach approximately USD 84.3 billion by 2032, supported by refresh cycles for EHR infrastructure, expansion of telehealth, and integration of real-world data into decision-making.

Within that, the United States market alone is expected to be worth about USD 76.6 billion by 2032, giving vendors and health systems a large and mature environment for advanced use cases such as AI-driven diagnostics, hospital-at-home models, and value-based care analytics.

Across these projections, the healthcare cloud market trends move from being a single budget line to a core environment where clinical, administrative, and analytical capabilities come together. Vendors, providers, and payers that build strategies around interoperable, secure, and scalable cloud architectures are positioned to capture a meaningful share of this growth.

Conclusion

The healthcare cloud computing market is already sizable, with strong double-digit growth, high adoption among providers and payers, and a clear path toward even greater scale through the early 2030s. Public, private, and hybrid deployment models support a mix of clinical information systems, non-clinical applications, and fast-growing service layers that help organizations modernize without rebuilding everything alone.

For technology leaders, clinicians, and payer teams, these statistics show that the cloud is now the default foundation for digital health. Strategic choices around architecture, governance, interoperability, and healthcare cloud management software development will determine how effectively organizations optimize performance, control costs, and unlock long-term value from a market that continues expanding in size, complexity, and opportunity.