Mobile wallets are changing the way people make payments around the world. They offer a fast, convenient, and secure way to pay for everyday purchases, transfer money, and manage personal finances. With the rise of smartphones and digital technology, mobile wallets are becoming an integral part of daily financial activities.

With the increased usage of digital wallets, industries and companies are changing to offer smooth mobile payment services. From retail and e-commerce to healthcare and transportation, mobile wallets have transformed the way transactions are done and are shaping the future of online payment.

Understanding Mobile Wallet

A mobile wallet is an online payment system that enables users to store, purchase, transfer money and conduct financial transactions using a mobile phone or any other device that has internet connectivity. These wallets are a safe, quick, and convenient alternative to money and physical credit cards.

The use of digital wallets has increased at a very high rate because of their convenience and ease of use. It allows users to make payments in just a few touches, scan codes, or authorize payments within seconds, which makes payment flow smooth in retail, e-commerce, transportation, and other markets.

Technological infrastructure and security features are also major factors in adoption. Mobile wallets are more widely available and accepted due to encryption, tokenization, and biometric authentication, as well as the high smartphone adoption, reliable internet access, and adoption by banks and fintech organizations.

Mobile Wallet Market Overview

The global mobile wallet market has evolved from a convenience-based alternative into the primary infrastructure of the modern financial economy. As of late 2025, the market is defined by a massive surge in total transaction value and a shift toward “Remote” cloud-based wallet solutions.

Global Market Valuation (2025–2026)

The industry’s financial health can be viewed from two main perspectives: wallet providers’ income and the total amount of money transferred through these systems.

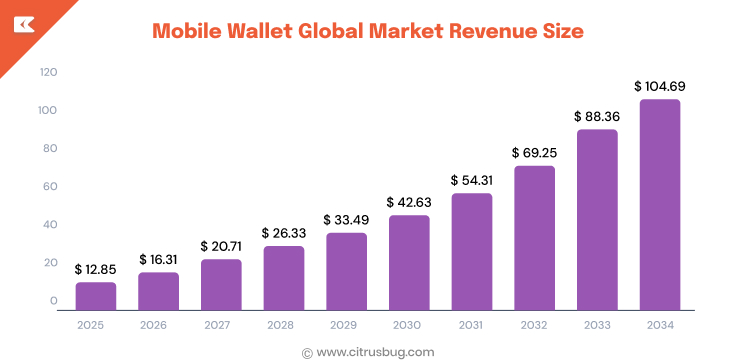

Market Revenue Size: TThe global mobile wallet market is estimated to be $12.85 billion in 2025. It is estimated to grow to $16.31 billion in 2026 at a Compound Annual Growth Rate (CAGR) of 26.3% through 2034.

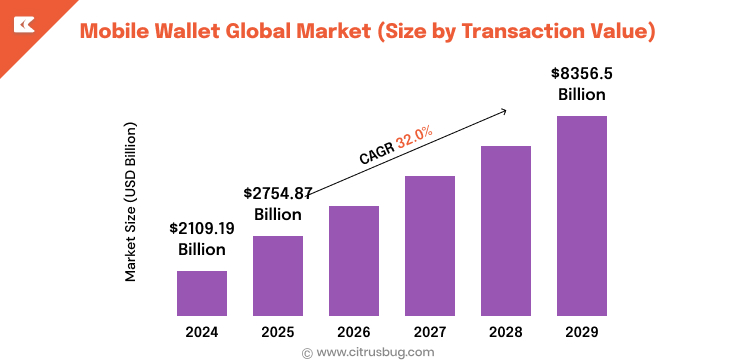

Total Transaction Value: The market is growing rapidly, with a significant increase in capital flowing through these platforms. According to data, global digital wallet transaction values are projected to rise from $2.1 trillion in 2024 to nearly $8.4 trillion by 2029.

Market Share by Technology:

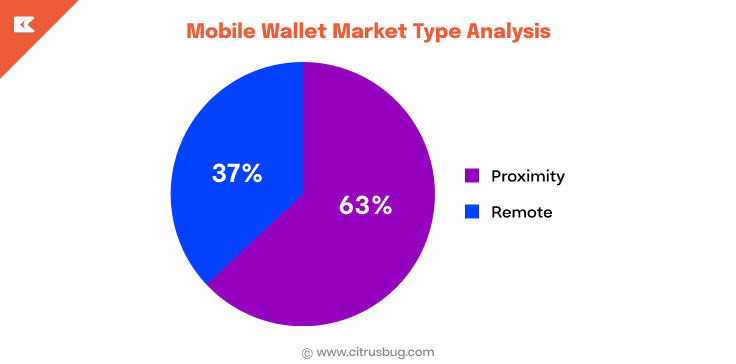

- Remote Wallets: Cloud-based and e-commerce wallets currently lead market growth with a projected CAGR of 28.7%.

- Proximity Wallets: NFC and tap-to-pay solutions remain the dominant physical payment method, holding an 86.8% share of the technology segment.

Global Mobile Wallet Usage Statistics and Adoption Rates

The transition from physical currency to digital interfaces has reached a global scale. As of late 2025, mobile wallets have officially moved from being an “alternative” payment method to the world’s most popular way to pay, both online and in-store.

Global Adoption Milestones (2025–2026)

- Total Global Users: Mobile wallet users have hit 5.2 billion by the end of 2025. This is more than 60% of the entire world population.

- Projected Growth: Growth is expected to exceed 5.3 billion users by 2026. Analysts project that by the year 2030, three-quarters of the world population will be regular users of digital wallets.

- Usage Frequency: In-app mobile wallets are set to capture 66% of global volume in 2025 due to the proliferation of thriving retail apps and embedded finance aspects.

- Transaction Share: eWallets have already surpassed over 50% of the global value of e-commerce transactions and about 30% of point-of-sale (POS) spending.

Usage by Generation

Adoption rates vary significantly by age, with younger generations viewing digital wallets as their primary financial tool, while older generations are increasingly adopting them for security and convenience.

| Generation | Adoption Rate (2025) | Key Behavior |

|---|---|---|

| Gen Z | 78.9% – 91% | The highest usage group, 41%, makes more than five transactions per month. |

| Millennials | 66.7% – 75% | Primary drivers of Peer-to-Peer (P2P) transfers and “Super App” engagement. |

| Gen X | 43.7% | Adoption is growing due to perceived safety and ease of Tap-to-Pay. |

| Baby Boomers | 25.7% | Least likely to adopt, though usage increased during 2024–2025 for online retail. |

[Source]

Leading Adoption Drivers

Two specific types of transactions are currently responsible for the bulk of new user growth:

- Peer-to-Peer (P2P) Payments: Nearly 84% of mobile wallet users now use their apps for P2P transfers, a massive jump from just 25% a few years ago. This is now the “entry point” for most new users into the digital ecosystem.

- QR Code Dominance: By 2026, QR code payments are expected to be the most popular transaction type globally, reaching 380 billion transactions and accounting for 40% of all digital wallet volume.

Financial Inclusion Impact

eWallets are currently the primary tool for financial inclusion in developing economies. According to the World Bank Global Findex (2025):

- Account Ownership: Mobile money platforms have helped boost global account ownership to 79% of adults.

- The “Unbanked” Opportunity: Nearly 900 million unbanked adults now own a mobile phone, providing a direct bridge for digital wallet providers to bring them into the formal economy.

Regional Mobile Wallet Statistics by Country and Market

The adoption of mobile wallets is not uniform; it is a tale of two worlds. In emerging markets, wallets are “leapfrogging” traditional banking, while in developed economies, they are steadily replacing physical cards through high-security NFC (Near Field Communication) technology.

Global Market Share by Region

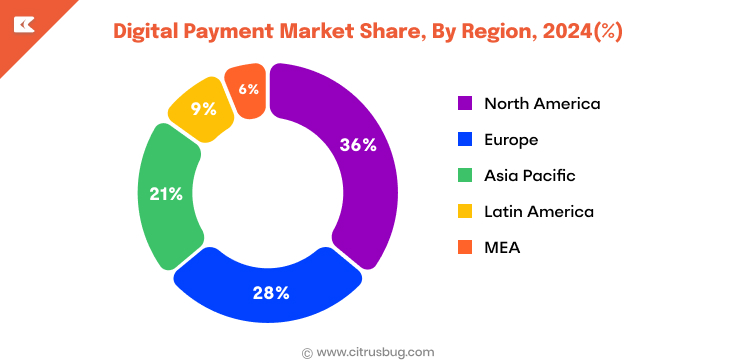

By the end of 2025, the Asia-Pacific region will remain the largest market, but Latin America and Africa will record the highest growth in new users.

[Source]

1. Asia-Pacific: The Global Epicenter

Asia remains the most mature mobile wallet market in the world, driven by a “mobile-first” culture where QR codes have almost entirely replaced cash in urban centers.

- China: With a 96% adult adoption rate, China is the world leader. The country’s digital payment transaction value reached $9.3 trillion in 2025, with Alipay and WeChat Pay still continuing to hold more than 90% of the market.

- India: India has the largest number of real-time transactions worldwide, with 46% of the total global real-time transactions. Unified Payments Interface (UPI) currently operates more than 16 billion transactions each month. PhonePe holds a dominant 45.9% share of the UPI market.

- Southeast Asia: Thailand, Vietnam, and the Philippines are projected to hit 75% adoption by 2026 due to the 311% growth in wallet usage in the past five years.

2. The Americas: The Rise of Real-Time & NFC

- United States: Wallet adoption is now mainstream, with 90% of customers having used a digital payment option within the past year. Apple Pay continues to be the dominant market player in the U.S., with 92% of all mobile wallets.

- Brazil: Brazil has become a global case study for digital transformation. Its Pix system, launched by the Central Bank, is projected to surpass credit cards in the online purchasing market share by the end of 2025, expected to capture 44% of all online payments.

3. Europe: Contactless Maturity

Europe’s market is defined by a high level of security and the integration of “Open Banking” that enables wallets to make direct contact with bank accounts without card intermediaries.

- United Kingdom: Contactless adoption has become effectively universal, with 94.6% of all card-present transactions being contactless in late 2024/early 2025.

- European Union: Digital wallets dominate online shopping in 14 leading European markets, and adoption is anticipated to cover more than 40% of all e-commerce transactions by 2026.

4. Africa & Middle East: Financial Inclusion

In this region, eWallets (often called “Mobile Money”) act as the primary bank account for millions.

- Sub-Saharan Africa: There are now over 1.1 billion registered mobile money accounts. In some nations, such as Kenya and Ghana, everything is done using mobile wallets, such as utility bills, government payouts, and so on.

- Middle East (MENA): The region is experiencing an accelerated change toward cash; digital wallets are set to replace 33% of all POS payments by 2027.

Industry-Specific Mobile Wallet Statistics

The use of mobile wallets has not been considered as a convenience feature anymore but rather as a necessity within the industry. Digital wallets are expected to reach 52.5% of the global value of e-commerce transactions by 2025 and become the leading mode of payment in the digital and physical storefronts.

The following are the specific statistics and trends that are fuelling the adoption in major sectors.

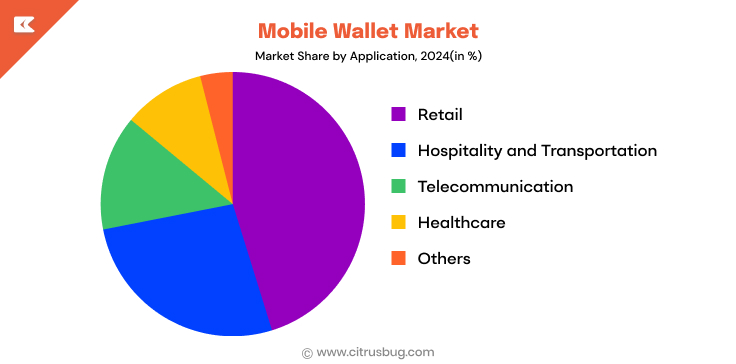

1. Retail and E-Commerce

Retail remains the largest market for mobile wallets, accounting for approximately 34% of the total market share in 2024.

- Conversion Power: The conversion rates of merchants with “one-click” mobile wallet checkout solutions are growing by an average of 30% compared to the same processes that demand manual card entry.

- In-Store Shift: 82% of retail merchants plan to increase or upgrade their mobile wallet acceptance capabilities by 2026.

2. Travel and Hospitality

The travel industry is going through a fast shift with customers demanding a frictionless journey.

- Essential Status: 74% of travelers now consider that digital wallets are essential for their trips.

- Usage Surge: The use of digital wallets to pay at travel-related locations (flights, hotels) increased by 20% to 28% between 2024 and 2025.

- Direct Booking: 54% of travelers choose to book directly with airlines using mobile applications instead of using third-party applications.

- Hospitality Efficiency: Hotels that have adopted mobile check-ins and digital keys record 23% more guest satisfaction and reduce front-desk processing time by 10 minutes to less than 3 minutes.

3. Gig Economy and Payouts

For the gig economy, mobile wallets have moved from a payment method to a critical infrastructure for worker retention.

- The “Instant” Expectation: Only 36% of gig platforms currently offer instant payouts; even among gig workers who haven’t yet used them, 94% prefer platforms that provide immediate access to earnings via e-wallets.

- Market Size: The global gig economy market was projected to reach $455 billion in 2025, with mobile wallets serving as the primary bridge for the unbanked and underbanked workforce.

4. Food, Beverage, and Delivery

Mobile wallets are the engine behind the $450 billion mobile food ordering industry.

- Higher Ticket Sizes: Customers spend 15–20% more per order when using an eWallet compared to physical card or cash transactions.

- Loyalty Integration: 78% of diners are willing to walk to a restaurant when they can earn rewards.

- In-App Dominance: Over 60% of quick-service restaurant (QSR) orders are now initiated or paid for via mobile devices.

5. iGaming and Gambling

The gambling industry utilizes mobile wallets to solve “speed of play” and security challenges.

- Market Value: The mobile gambling market is estimated to reach $105 billion in 2025.

- Engagement: Players using mobile-integrated wallets show 30–40% higher engagement levels due to the ease of deposits and “instant” withdrawals.

- Casino Shift: In the U.S., mobile casino games already account for roughly 62% of online gambling revenue.

6. Public Transit and Transport

Transit is often the “gateway” for daily mobile wallet habits.

- CAGR Growth: Transaction volume for transit and toll payments is expected to grow at an 8.3% CAGR between 2025 and 2030.

| Industry | Projected Market Value | Mobile Wallet Penetration | Key Driver |

|---|---|---|---|

| E-Commerce | $7.5 Trillion | 52.5% | One-click checkout |

| Gig Economy | $455 Billion | 65% (Payouts) | Instant earnings access |

| Travel | $1.1 Trillion | 28% | Frictionless airport/hotel experience |

| Food Delivery | $450 Billion | 60%+ | High-frequency usage |

Global Merchant Acceptance Rates Statistics

By late 2025, the difference in acceptance between online and physical stores became much smaller with the coming of standard point-of-sale (POS) hardware with NFC and QR support.

- Retail Expansion: 82% of merchants around the world intend to increase the ability to accept digital wallets by the end of 2025 to satisfy the growing demand.

- Small Business (SMB) Adoption: Approximately 49% of the Small and Medium Businesses currently accept mobile wallets, the highest in the history of the technology, following the low cost of mobile POS (mPOS) solutions such as Square and Toast.

- E-commerce Integration: Roughly 66% of the total number of e-commerce merchants currently integrate at least one digital wallet into their checkout process. Among digital-centric merchants (merchants receiving more than half their revenue online), the rate of integration increases to 70-71%.

Mobile Wallet Security, Fraud, and User Trust Statistics

In 2025, the security landscape of mobile wallets is defined by a paradox where technically superior protection coexists with a surge in sophisticated, identity-based threats.

-

Tokenization as a Core Defense

Approximately 93% of leading mobile wallets now utilize tokenization to replace sensitive 16-digit card numbers with unique digital identifiers. Businesses adopting this technology report a 34% drop in payment fraud compared to traditional security measures.

-

Biometric Adoption and Confidence

Global biometric payment transactions are expected to reach $3 trillion this year. As of today, 81% of users claim that they feel safer when they use FaceID or fingerprint recognition instead of physical cards because those technologies have a multi-factor protection mechanism built in.

-

The Shift to Mobile-Centric Fraud

Since physical card skimming has decreased, criminals have shifted to online victims. In 2025, about 75% of world digital payment frauds are expected to be on mobile devices, with overall fraud losses estimated to amount to $50 billion globally.

-

Emerging AI and Identity Threats

Synthetic identity fraud, meaning using AI to make completely fake personas, has increased by more than 100% since 2022. Also, “Quishing” (fraudulent QR codes) has experienced a growth of 51% in 2025 since it is an initial method of social engineering.

-

Generational and Regional Trust Gaps

While 81% of Gen Z consumers consider biometrics the most secure identity verification method, overall trust varies significantly by region. Only 65% of U.S. consumers have adopted digital wallets daily compared to 93% in China and over 80% in Brazil.

Future Trends in Digital Wallets

The mobile wallet ecosystem is moving into an era of more intelligence, wider functionality, and closer integration with daily digital experiences. Other than payments, digital wallets are becoming complete financial platforms.

AI-Driven Personalization & Fraud Prevention

Real-time fraud detection, spending insights, and predictive alerts will continue to be driven by artificial intelligence. Wallets will study user behavior in order to tailor their offers, automate their budgets, and eliminate suspicious transactions in real-time.

Rise of Super Apps and Embedded Finance

Digital wallets will further combine payments, banking, lending, insurance and investments into one platform. Embedded finance will enable users to gain access to financial services directly within the retail, travel, healthcare, and gig-economy applications.

Expansion of Real-Time and Cross-Border Payments

Instant payment rails such as UPI, Pix, and FedNow will become available around the world and allow quicker wallet-to-wallet transfers across borders. This will minimize the use of cards and decrease transaction costs to the businesses and consumers.

Growth of QR, Wearables, and IoT Payments

QR codes will take over new markets, whereas wearables and IoT-based payments will become popular in developed markets. Connected cars, smartwatches, and biometrics will allow a smoother and passive use of wallets.

Stronger Digital Identity and Compliance Layers

Wallets will play a central role in digital identity management. Verifiable credentials, decentralized identities, and biometric authentication will enhance trust and assist businesses in achieving changing regulatory and KYC standards.

Conclusion

Mobile wallets are no longer just a convenient payment option. They are now the foundation of the global digital payments system. As used by billions of customers, with transaction value exceeding trillions of dollars, and being extensively adopted by various sectors, digital wallets are transforming the way individuals store money, shop, and engage with financial services.

With the further development of AI, real-time payments, and embedded finance, the need to develop secure and scalable digital wallet apps will grow. Companies investing in tailored eWallet solutions can enhance consumer confidence, simplify processes, and open new business avenues. It is now crucial to adjust to a wallet-first future to remain competitive in the changing digital economy.