Introduction

Technology is changing how insurance is priced, sold, and serviced. Tasks that once took days now take minutes because of automation, AI tools, and digital platforms. The customers desire quick claims, transparent pricing, and mobile services, and this is why the way that insurers operate is improving.

InsurTech statistics help explain this shift. They show where the market is growing, which tools are being adopted, and what improves performance. This report highlights key trends in tech spending, digital adoption, regional growth, and fintech app security.

What Is InsurTech?

InsurTech refers to using technology to make insurance faster, easier, and more efficient. It substitutes manual time-consuming processes with automated and data-oriented processes.

Common examples of InsurTech solutions include AI for detecting fraud, automated underwriting solutions, digitally based claims management systems, policy documentation systems and customer self-service applications. In addition, Insurers use cloud-based computer systems and data analytics to design flexible insurance products and make informed decisions.

Global InsurTech Market Overview (2026 Snapshot)

Market Size and Growth

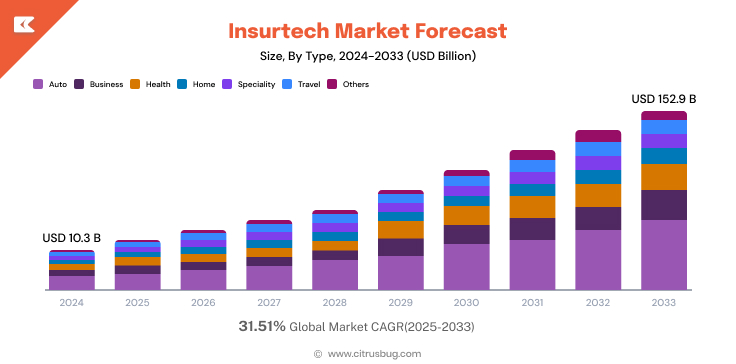

Current estimates place the global InsurTech market at approximately USD 19.2 billion in 2025. Assuming similar continuous growth based on continued digital adoption, market value is projected to grow to USD 22.64 billion by 2026.

Longer term, there are multiple forecasts indicating strong growth as evidenced by a widely referenced report projecting the InsurTech market to reach USD 152.9 billion by 2033 with a CAGR of 31.5% from 2025 to 2033.

This expansion indicates rising use of online insurance systems, the need to automate, and customer shifting demands. Technology, and AI, cloud, IoT, data analytics, in particular, is becoming complex enough that people and technology companies are creating systems that are more efficient, scalable, and accessible to customers.

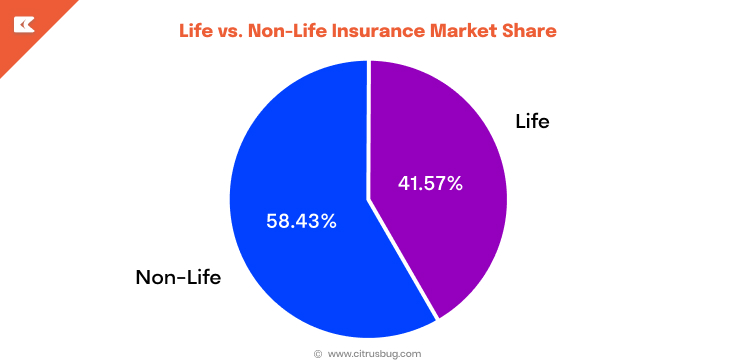

Life vs. Non-Life Segments

Although precise splits exist between life vs non-life in the world depending on the source of the report, the trend across the board remains strong with InsurTech investment under both categories. Non-life will be more likely to be on the frontier of the rate of adoption (because of the speedy feedback loops), whereas life/health segments are becoming more and more investment-friendly to grow over time.

- The insurance market in the world is still skewed towards non-life products. In 2024, the non-life insurance covered approximately 58.43% of the overall market. This is in the form of auto, property, health and commercial cover.

- Life insurance continues to grow steadily. Reports show the life segment is expanding at a projected 5.45% CAGR through 2030 as demand for long-term protection and savings products increases.

- Life insurance is increasing steadily. It has been reported that the life segment is growing with a projected CAGR of 5.45 over the coming years to 2030 due to the growth in the demand of long-term protection and savings products.

- Regional patterns vary. Life insurance is more organized in the Asia-Pacific region, comprising approximately 61.3% of the total life, as well as non-life insurance premiums in 2024.

The figures indicate the variability of market balance across geography and the demand of a product and allow insurers to better strategize their products.

Key Forces Driving Market Expansion

The expansion of InsurTech is being stimulated by a number of critical drivers around the world:

- Digital transformation at insurers: Most traditional carriers are swapping out old systems with new ones – enhancing speed, flexibility and scalability. The implementation of cloud, analytics, and digital workflows minimize the number of manuals and enhance the quality of the services.

- Customer demand for convenience and transparency: The increasing consumer expectation of convenient digital solutions, such as mobile purchasing, real-time quotes, fast claims, etc., is compelling insurers to implement InsurTech solutions.

- Emerging markets and under-penetrated segments: Countries in the Asia-Pacific (APAC) region have a large number of consumers who are still uninsured or under-served. Therefore, mobile-first products in the form of affordable micro-insurance are key avenues for growth.

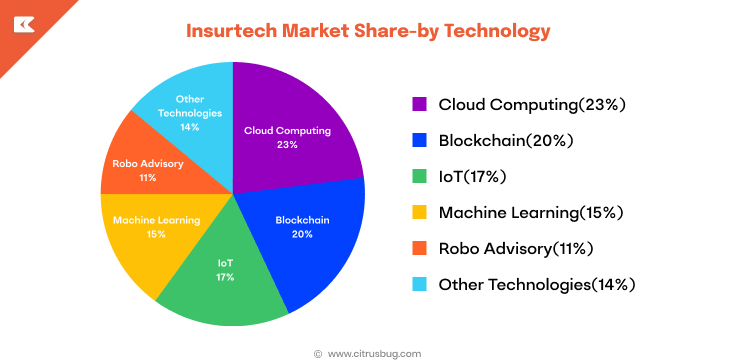

- Technology innovation: AI, IoT, data analytics: Advanced technologies for risk scoring, telematics in real estate, and automated claims processing provide opportunities to create new usage-based and dynamically priced, on-demand insurance products.

- Regulatory shifts and open-ecosystem adoption: In some markets, regulatory reforms, open-insurance frameworks, and increased support for tech-driven insurance products encourage InsurTech adoption by both incumbents and new entrants.

- Partnerships and embedded distribution: Insurers are partnering with other technology companies, brokers and distributors outside of the insurance industry, to create a larger distribution network and reduce operational costs. This increases the availability of insurance particularly in non- traditional markets. This trend also favors the models of embedded insurance as they promote the need for flexible integration and recent platforms.

What This Snapshot Suggests for 2026

According to recent statistics and growth drivers, it is expected in 2026 that:

- Further growth in the size of the global market, modest growth with 2025, and additional growth in the next coming years.

- Strong leadership by North America and Europe in absolute size, while APAC gains share rapidly thanks to emerging markets and digital adoption.

- The absolute size of the leadership of North America and Europe, plus the fact that APAC is capturing a lot of share, with the help of emerging markets and the shift to digital.

- Even growth in both life/health and non-life business though non-life can dominate in the short run with fast feedback loops.

- Additional advancement of AI, data-driven underwriting, cloud-based solutions, telematics, and embedded distribution.

- Increased integration of the traditional insurers, InsurTech sellers, fintech businesses, and non-insurance platforms – implying more of an ecosystem than individual tech vendors.

This section offers a high-level view. Further on, we will discuss funding trends, insurer adoption rates, product mix changes, claims automation and fraud detection, and security concerns all supported by the necessary InsurTech statistics and resources.

Investment and Funding Statistics

Cumulative Funding Milestone

Total funding for InsurTech since 2012 reached about USD 60.8 billion (reported in Q2 2025).

Quarterly Totals and Deal Counts

Q2 2025 funding was USD 1.09 billion across 91 deals; average deal size that quarter was about USD 12.83 million.

Q3 2025 recorded USD 1.01 billion in funding with 76 deals, the lowest quarterly deal count since Q2 2020.

Capital Concentration by Theme

AI and analytics dominated recent rounds. In Q3 2025 roughly 74.8% of InsurTech funding went to AI-centred companies. Others on the list of the highest categories are embedded insurance, claims automation, and health-tech platforms.

Deal-stage and VC Behavior

Venture capital has shifted toward later-stage, revenue-generating startups; seed rounds are tighter and smaller compared with the 2019–2021 boom. Investors increasingly require clear unit economics and enterprise readiness.

Corporate and Insurer Participation

Corporate investment in insurers and re-insurers increased, with the Q3 2025 recording a high count of corporate-supported deals as companies want strategic technology abilities and distribution connections.

[Source]

Technology Adoption Statistics

AI/ML Adoption in Underwriting and Claims

- The insurance segment of the AI market was estimated at approximately USD 10.24 billion in 2025, with a CAGR of approximately 32.8%.

- The use of AI/ML solutions by many insurers has become standard. According to one survey, over 82% of insurers today use AI to process claims, and the workflows powered by AI are on average many times faster in claims-processing.

- These solutions enhance the quality of decision-making, AI-based insurers state better risk assessment, faster processing, and reduce the number of manual mistakes.

Cloud, API, and Digital Platform Adoption

- Approximately 68% of insurers in the world have embraced cloud computing platforms to facilitate business functions such as administration of policies, infrastructure capable of scaling and digital services.

- Since digital transformation, more insurance companies are basing their providers on API platforms or SaaS applications – allowing access to partner systems, third-party applications and digital distribution channels more easily.

Automation and Workflow Digitization

- Approximately 61 percent of insurance companies indicated use of digital self-service portals to policyholders; this facilitates policy management, renewal and initiation of claims by use of web or through mobile channels.

- Automated document processing — replacing manual paperwork — is in use at about 68% of organizations.

- Digital transformation initiatives have also lowered the processing time: numerous insurers that work with digital processes have noted decreased time spent by the company on policy servicing, claims adjudication, and responding to customers.

Operational Efficiency Statistics

Faster Digital Underwriting

- According to many underwriters who have automated, there is a substantial increase in speed. AI-based underwriting may cut the time of underwriting by 50%.

- Another advantage is increased accuracy: machine-learning underwriting and risk models enhance the risk assessment and minimize the mistakes as compared to manual underwriting.

Automated Claims Processing Improvements

- In firms that have an advanced digital workflow, claims processing time has reduced drastically. Legacy manual systems result in some being reduced by upto 70 percent.

- Practically, the insurers with AI-powered claims systems tend to pay smaller claims within hours, instead of days.

- Also, there is a reported reduction of administrative cost of approximately 30% in case claims and document processing is automated.

Fraud Detection, Processing Times, and Cost Savings

- AI-based fraud detectors are much better at detecting fraud. According to most companies, fraud detection rates have increased by up to 78 percent with the implementation of machine learning systems.

- This has improved detection to save large sums around the world; it is estimated that AI fraud-detection could save USD 7.5 billion to insurers all over the world in 2025.

- Investigating and adjusting fraudulent and erroneous payouts reduces the cost of these processes as well, which, in turn, helps insurers to maintain healthier loss ratios and invest in innovation.

Efficiency Gains Across the Insurance Value Chain

- In addition to underwriting and claims, insurers who have digital solutions report general efficiency: some 78% of companies indicate that digital change enhanced the overall operation performance.

- Routine activities such as document review, data entry, customer onboarding, renewals and policy administration are becoming more automated thereby lessening the manual labor and shortening the turn around time across the board.

- Consequently, insurers are able to handle more policies and claims with less resources improving throughput and reducing the cost per transaction. This is scalable efficiency that helps in the growth and competitiveness in a developing industry of insurance.

Customer Behavior & Experience Statistics

Digital Channel Usage and Self-Service Adoption

- Many customers now prefer to interact with insurers through digital channels rather than traditional agents. According to a 2025 report, about 70% of insurance customers prefer digital channels over traditional agents.

- Over 54 percent of the insurance policies were being sold online in 2025 as the purchase moves towards a digital direction.

- Moreover, 55 percent of clientele utilize the digital self-service portals in management of their policies, which shows the increased adoption of self-service tools.

Mobile & Omnichannel Usage

- Omnichannel and mobile access have been introduced into insurance. As an illustration, 69% of insurance clients like mobile applications in policy management.

- More so, 60% of insurance claims are currently made through mobile applications, which signify movement toward mobile-based claim filing and customer points.

- The customers also demand various forms of communication: many customers demand to gain access via such channels as web portals, mobile applications, chat or telephone, rather than through the conventional agent-based channels.

Customer Expectations: Speed, Personalization, Transparency

- Modern insurance customers often expect services to be fast, personalized, and transparent. In a 2025 study, 78% of customers said quick responses improve their overall satisfaction.

- Approximately three out of every four consumers indicated that they will be willing to purchase insurance products with companies that provide them with personalized experiences.

- Regular updates are also expected by many customers e.g. proactive status updates about claims or policy renewals not waiting.

Customer Satisfaction: Digital vs Traditional Journeys

- Digital experiences may enhance satisfaction in an event where they are carried out effectively, but various customers incline to hybrid models. A 2025 survey from a major provider found only 15% of consumers want a fully digital-only insurance journey.

- In the meantime, 48% of the respondents that year in that survey wanted a digital-first system with a possibility of reaching out to a person when necessary, meaning that they would need both convenience and human touch.

- Also, 60% of insurance consumers say they want self-service options available 24/7, again showing demand for digital convenience on customers’ terms

Customer Retention and Loyalty Linked to Digital Experience

- Online activity appears to increase loyalty. Studies indicate that customers who have no digital hassles will remain loyal to their insurer 4 times more.

- In addition, insurers indicate that digital communication and online service boost retention – 55% of insurers in a 2025 study indicated that online digital communication and online service helped to boost retention.

- Consumers too are more open to switching whenever they feel that they have a poor digital experience: in a report, 52% of insurance consumers indicated that they could change providers to gain better digital experiences.

[Source]

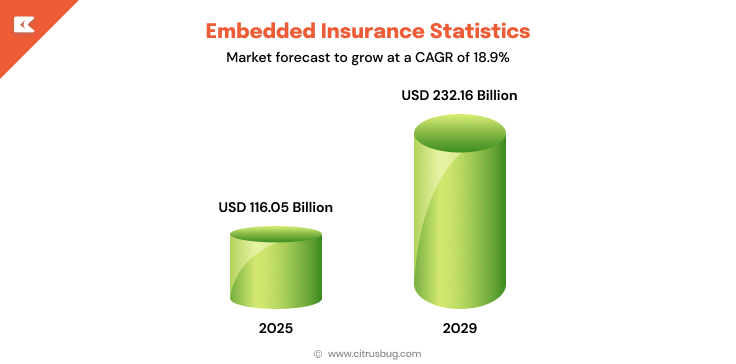

Embedded Insurance Statistics

Market Growth

Embedded insurance is increasing at a high rate. The market will increase to 116.05 billion in 2025 as compared to 97.57 billion in 2024 at a compound annual growth rate (CAGR) of 18.9%.

Adoption Patterns

Channel conversion rates: standard offers are attached at 5-15% and targeted flows such as device protection are above 20%.

Emerging Platforms

Embedded insurance is gaining more and more popularity with major e-commerce, mobility, and fintech platforms using APIs. A high demand is being witnessed in companies specialized in the development of insurance software solutions.

Popular Product Types

Embedded offerings are mostly dominated by device protection, travel insurance, short-term health and add-on warranties. Fast and convenient underwriting and automated platforms are in place.

Regional InsurTech Statistics Breakdown

North America

- Market share: the largest in the world, approximately 38-39 percent of all InsurTech revenues.

- Adoption: high adoption of AI underwriting, telematics, and digital claims.

- Ecosystem: high level of startup activity, and various unicorns.

Europe

- Regulation: GDPR and open-insurance frameworks shape growth.

- Leading markets: UK, Germany, Nordics.

- Enterprise adoption: the main procurement requirements are compliance and fintech apps security.

APAC

- Growth: fastest-growing InsurTech region, high CAGR.

- Digital-first adoption: mobile payments and penetration of smartphones lead to adoption.

- Distribution: Distribution and embedded and platform sales, such as the integration of fintech apps.

Middle East & Africa / LATAM

- Emerging trends: micro-insurance, mobile distribution, regulatory sandboxes.

- Opportunities: high growth potential in underinsured segments, simplified onboarding and local partnerships.

Key Opportunities by Region

- North America: Automation of AI and claims.

- Europe: trust is motivated by regulatory compliance.

- APAC: scale of embedded insurance and micro-insurance.

- MEA / LATAM: mobile-first adoption, simplified KYC.

Future Outlook: What 2026 Indicates About the Next Phase

Expected Growth Areas

InsurTech market has been estimated to be over USD 20 billion by 2026 with the sectors of AI-based underwriting, online claims service and health insurance technology being the core growth areas.

Some of the new trends are embedded insurance, micro-insurance in the APAC, and platform-based distribution in North America and Europe.

Role of AI, Automation, and Analytics

Adoption of AI is on the increase: more than 82 percent of insurance companies apply AI/ML in claims and risk evaluation.

Automation and analytics will shorten the processing time by 50-70 percent, increase the accuracy of the fraud detection process by 78%, and decrease the operational costs by up to 30 percent.

Insurance fraud detection software development and workflow digitization platforms will remain the essential investment areas.

Predictions for Underwriting, Claims, and Customer Experience

- Underwriting: The introduction of dynamic pricing and risk scoring due to AI will be the norm with quicker approvals.

- Claims: There will be more high-volume claims which will undergo the digital and automated claims processes with minimal human intervention.

- Customer Experience: Personalized, omnichannel engagement will dominate, with mobile self-service adoption rising above 60% in key markets.

Partnerships Between Insurers and Tech Companies

Cooperation will be quicker: additional insurers will collaborate with InsurTech startups, fintech platforms, and embedded distribution providers to increase offerings. Strategic alliances help to support integrated product ecosystems, improve digital delivery and speed up the time-to-market.

Conclusion

According to the InsurTech statistics 2025-2026, the industry is heading resolutely in the automation, digital platforms, and AI-driven operations direction. Technology adoption has tangible benefits in the form of operational efficiency, quicker underwriting and enhanced fraud detection.

To companies, it means that the opportunities of digital insurance are ceasing to be experimentation. The companies investing in health insurance software solutions, automating their workflows, or distributing via a platform can achieve their objectives of customer engagement, lower cost, and compete successfully in a market that is changing rapidly.

The growth of markets, regional expansion, use of technology and partnerships have all made it clear that 2026 will mark the beginning of the next, more integrated phase of global InsurTech.