The DevOps automation tools market has expanded at a rapid pace as organizations prioritize faster software delivery and more efficient infrastructure management. Automation platforms for CI/CD pipelines, configuration management, testing, and deployment have moved from optional enhancements to core operational requirements for modern development teams.

Enterprises of all sizes are increasing their investment in delivery and infrastructure automation to reduce manual intervention, improve deployment frequency, and maintain reliable release cycles. Cloud adoption, microservices architectures, and the growing complexity of IT environments continue to accelerate this transition across both mature and emerging technology markets.

Market data from 2025 and 2026 reflects strong momentum in global valuation, enterprise-level adoption, and regional expansion. High-maturity organizations are now reporting measurable gains in deployment speed and incident response. The market trajectory points toward sustained growth through the end of the decade, supported by rising cloud spend and the growing importance of MLOps tools and platforms in operational workflows.

What Are DevOps Automation Tools?

DevOps automation tools are software platforms that automate tasks across the software development lifecycle. They handle code integration, testing, deployment, infrastructure provisioning, and monitoring to help teams deliver software faster with fewer errors. These tools reduce the manual effort needed to manage complex IT environments. By standardizing workflows and enabling continuous delivery, they allow organizations to scale operations, respond to incidents faster, and maintain consistent software quality.

DevOps Automation Tools Market Size and Valuation

The global market for pipeline and infrastructure automation tools has grown significantly over the past two years. Enterprise demand for faster and more reliable software delivery has driven aggressive investment across all major industries. Current valuations reflect the depth of this adoption, and the pace of expansion shows no signs of slowing as organizations continue to standardize their DevOps toolchains and extend them into new areas like security and compliance.

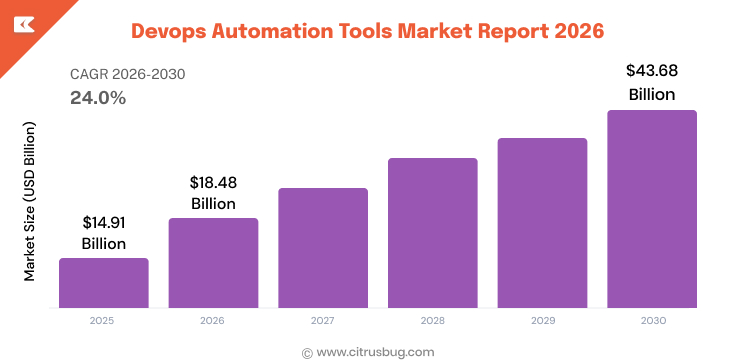

Global Market Valuation (2025 to 2026)

The market has shown strong year-over-year expansion from 2025 to 2026. Rapid cloud migration, container adoption, and the growing use of microservices architectures have all contributed to this acceleration.

- Market value grew to $14.91 billion in 2025. The increase reflected a sharp rise in cloud-based tool adoption, broader enterprise-level rollouts of DevOps practices, and deeper integration of automation into existing IT workflows.

- The market reached $18.48 billion in 2026 at a compound annual growth rate (CAGR) of 23.9%. Cloud infrastructure expansion, continuous delivery mandates, and the rise of platform engineering teams are the primary contributors to this growth trajectory

Component and Segment Breakdown

Software solutions and continuous integration tools are among the most actively adopted categories in the market, reflecting broader DevOps trends. Their performance provides a clear picture of where enterprise budgets are being allocated and which parts of the DevOps toolchain are receiving the most attention.

- The solutions segment held 59.65% of the total market share in 2025. Enterprises continue to prioritize ready-made automation platforms over custom-built alternatives due to faster implementation timelines and lower maintenance overhead.

- Continuous integration tools were independently valued at $1.35 billion in 2024. Build and test automation capabilities remain a foundational layer for DevOps toolchains, and most organizations treat CI as the first step in their automation journey.

Adoption and Usage Statistics Across Enterprises

Toolchain-driven delivery has moved beyond early adopters and into mainstream enterprise operations. The majority of large organizations now maintain active DevOps pipelines, and the efficiency gains they report are reinforcing continued investment. Smaller organizations are also entering the market as SaaS-based tools lower the barrier to entry.

Enterprise-Level Investment and Penetration

Large enterprises are the primary consumers of these tools, and their spending patterns set the pace for the broader market. Their requirements for multi-cloud orchestration, compliance workflows, and infrastructure design services are driving much of the current innovation across the vendor landscape.

- Over 65% of enterprises have invested in pipeline and delivery automation tools. The push for faster release cycles and operational efficiency has made these platforms a standard budget line item across IT departments, particularly in industries with high deployment frequency.

- Large enterprises accounted for 64.05% of total market revenue in 2025. Their scale of operations and multi-cloud environments require comprehensive automation coverage across the full development lifecycle to maintain reliability and speed.

Efficiency and Delivery Outcomes

The impact of these tools on software delivery is measurable and well-documented across organizations of varying maturity levels. Organizations that have implemented full toolchain integration report shorter release cycles, fewer failed deployments, and better cross-team visibility.

- More than 70% of organizations report increased software delivery efficiency through DevOps toolchain integration. Faster feedback loops, automated testing, and streamlined deployments are the primary drivers behind these gains.

- Organizations at higher maturity levels report the most consistent improvements, particularly in industries like financial services, telecommunications, and healthcare, where release frequency directly impacts service quality, customer retention, and regulatory standing.

Regional Market Share and Growth Insights

The use of pipeline and infrastructure automation is growing worldwide, but not at the same speed everywhere. North America leads the market because it has strong cloud systems and high IT spending by companies. On the other hand, the Asia Pacific is growing the fastest, with more businesses adopting new tools and investing in cloud-based technologies.

North America

- North America holds over 37% of the global market share as of 2025. The region has strong cloud systems, many technology companies, and large IT budgets that are focused on automation and improving platforms. Revenue from this region is expected to surpass $25 billion by 2032, supported by continued adoption across financial services, healthcare, and government sectors where regulatory compliance requirements are accelerating investment.

Asia Pacific

- The Asia Pacific region is expected to grow the fastest, with a yearly growth rate of about 20.2%. Rapid digital growth in India, China, Japan, and Southeast Asia is increasing the need for DevOps platforms, as both large companies and startups build cloud-based applications. Government-backed technology modernization programs, a growing pool of skilled developers, and the expansion of local cloud data centres are additional accelerants in the region.

Europe

- Germany is projected to generate $1.13 billion in cloud-based automation tools revenue by 2031. Europe’s broader adoption is driven by digital transformation mandates in financial services and automotive industries, where speed to market and software reliability are critical competitive factors. Strict regulatory frameworks around data privacy, such as GDPR, are also motivating the use of DevOps tools that support compliance automation, audit trails, and policy-as-code implementations across enterprise environments.

Market Segmentation Insights

The broader market is composed of multiple segments that serve different organizational needs. Deployment models, component types, and organization sizes all shape how businesses adopt and scale their strategies around continuous delivery and infrastructure management. Each segment follows its own growth pattern based on the specific demands and budgets of the organizations it serves.

Cloud-First Deployment Preferences

Public cloud deployment has emerged as the preferred model for these platforms, particularly among organizations with distributed teams and multi-region infrastructure needs.

The public cloud segment accounted for 44.70% of the total market size in 2025. Cloud-native tools offer faster setup, lower upfront costs, and better scalability compared to on-premise alternatives. This preference is especially strong among mid-sized companies and fast-scaling startups that need to provision environments on demand without managing physical hardware.

Infrastructure and App Release Automation Components

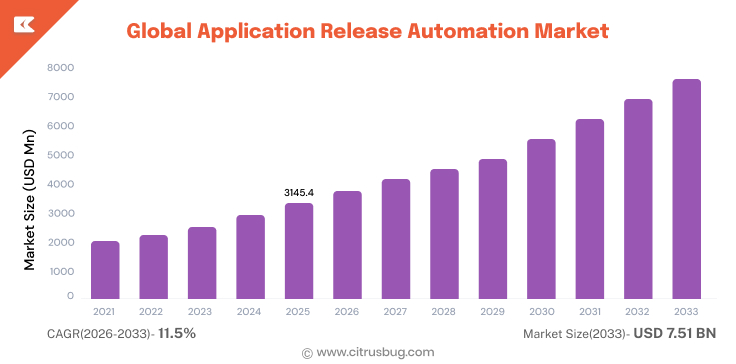

Within the DevOps toolchain, infrastructure-as-code (IaC) and application release automation (ARA) are two high-growth segments that are reshaping how enterprises manage provisioning and deployment processes.

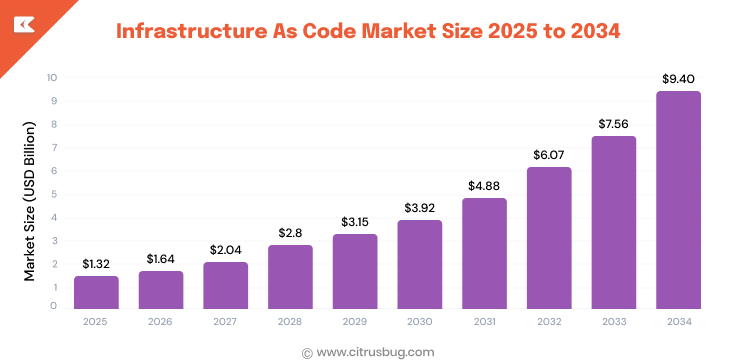

Infrastructure as Code Market:

The global IaC market was valued at around $1.06 billion in 2024 and is expected to grow significantly to nearly $9.40 billion by 2034, with a strong growth rate of 24.39% during the forecast period. North America accounted for about $360 million in 2024, showing strong regional adoption.

This growth is driven by increasing demand for cloud services, rising adoption of DevOps practices, better security requirements, cost efficiency, and the use of advanced technologies. Tools such as Terraform, Pulumi, and AWS CloudFormation continue to play an important role by enabling consistent, version-controlled infrastructure management and reducing configuration issues.

Application Release Automation Market:

The ARA segment is also growing steadily, with a projected CAGR of 11.5% between 2026 and 2033. As release pipelines become more complex and involve multiple microservices and environments, ARA tools help automate deployment coordination across staging, testing, and production.

Growth Among Small and Medium Enterprises

While large enterprises currently dominate the market, small and medium enterprises (SMEs) are closing the gap at a notable pace as SaaS platforms reduce cost barriers.

The SME segment is expected to grow at a CAGR of 18% during the forecast period. Affordable SaaS-based DevOps platforms, pay-as-you-go pricing models, and reduced infrastructure requirements are making automation tools accessible to smaller organizations. This trend is particularly visible in cloud-first economies where SMEs are building digital products from the ground up and need efficient delivery pipelines from day one.

Key Trends in DevOps Automation

The DevOps tooling landscape is evolving fast, with new practices and platform capabilities reshaping how teams build, test, and deploy software. The trends driving this evolution go beyond tooling upgrades and reflect deeper shifts in organizational maturity, operational strategy, and the role of AI in modern software development.

1. Widespread Plans for Automation Platform Upgrades

Automation is no longer a differentiator but a baseline expectation for engineering organizations. One industry report found that 86% of teams plan to add new or upgraded automation platforms in the near term.

This includes investments in pipeline orchestration, automated compliance checks, and self-service developer environments. The emphasis is on reducing manual toil and enabling developers to focus on shipping features rather than managing infrastructure or waiting on approval workflows.

2. AIOps and Intelligent Monitoring

Artificial intelligence is becoming embedded in DevOps monitoring and incident management workflows. The AIOps market is growing at approximately 15% compound growth per year, driven by the need for smarter observability at scale.

AI-powered tools now analyze logs, metrics, and traces in real time to detect anomalies before they escalate into full-outages. Predictive alerting and automated root cause analysis are two of the most adopted capabilities. These features are particularly valuable for organizations with large-scale distributed systems where manual monitoring is no longer practical.

3. Deployment Automation at Scale

Mature organizations are pulling ahead by automating a greater share of their deployment processes. High-maturity organizations are 36% more likely to automate the majority of their deployments compared to lower-maturity peers. This gap reflects a deeper investment in release orchestration, canary deployments, and rollback automation.

The result is faster time-to-production with fewer manual handoffs and reduced risk during releases. Teams at this level of maturity typically manage hundreds or thousands of deployments per week with minimal human intervention.

4. Improved Incident Response Through Automation

The benefits of DevOps maturity extend well beyond deployment speed into operational resilience. Those same high-maturity teams are 66% more likely to respond “very effectively” to production incidents.

Automated runbooks, integrated alerting systems, and chaos engineering practices are enabling faster recovery and lower mean-time-to-resolution across production environments. For organizations in regulated industries or those operating mission-critical systems, this level of operational control has become a key factor in maintaining customer trust and competitive positioning.

Factors Driving Market Growth of DevOps Automation

Several structural and operational trends are pushing the broader tooling and automation ecosystem forward. These factors are not short-term catalysts but long-standing shifts in how organizations build, deploy, and maintain software systems. Each trend reinforces the others, creating a compounding effect on market expansion.

1. Accelerating Demand for Continuous Delivery

The need for faster, more reliable software releases has made pipeline and delivery automation a strategic priority across industries. The broader market has maintained a 20% compound annual growth rate over recent years.

As product teams adopt agile methodologies and CI/CD pipelines at scale, the demand for tools that orchestrate these workflows has become constant. Organizations in retail, finance, and healthcare are among the most aggressive investors in delivery automation, driven by customer expectations for frequent updates and stable digital experiences.

2. Rising Need for Professional DevOps Services

As organizations mature their DevOps practices, the demand for implementation, consulting, and managed services is growing alongside the tools themselves. The DevOps service market is expected to register a CAGR of approximately 25.2% through 2030.

Enterprises increasingly rely on external expertise to integrate and optimize automation tools across complex hybrid environments. This services layer is becoming a key revenue driver for vendors and consultants, especially in regions where in-house DevOps talent remains scarce.

3. Proven Growth Trajectory Over Multiple Cycles

The market has demonstrated consistent expansion over several investment cycles, with a documented CAGR of 19.1% through 2026. Organizations that adopted DevOps early are now expanding their toolchains into areas like security automation, policy-as-code, and platform engineering.

This compounding effect of maturity-driven expansion continues to widen the total addressable market year over year, and it provides confidence for new entrants and late adopters to commit resources.

Future Outlook and Market Projections

The global market is positioned for sustained long-term growth as enterprises deepen their investment in software delivery infrastructure. Near-term projections through 2030 and extended forecasts through 2032 point to a market that could more than quadruple its current valuation within the next several years. Both the core tooling segment and the broader DevOps ecosystem are expected to scale substantially as organizations embed automation across every stage of the software lifecycle.

Projected Market Growth Through 2032

Strong enterprise investment and expanding tool ecosystems are expected to sustain above-average growth rates through the early 2030s. Cloud migration, platform engineering, and the maturation of DevSecOps practices are all contributing to an outlook that remains bullish across all major forecasting models.

- The global DevOps automation tools market is projected to reach $43.68 billion by 2030 at a CAGR of 24%. Pipeline standardization, infrastructure-as-code adoption, and the proliferation of internal developer platforms will remain the primary growth drivers through the end of this decade. Organizations in healthcare, finance, and e-commerce are expected to be among the largest spenders.

- By 2032, the market is expected to grow to approximately $72.81 billion with a CAGR of 26%. The acceleration is driven by rising adoption in mid-market enterprises and emerging economies that are scaling their digital infrastructure rapidly. Increased focus on developer productivity and self-service tooling is also expected to widen the total addressable market.

- The on-premise deployment segment alone is forecast to reach $45 billion by 2032. Regulated industries such as banking, defense, and healthcare continue to demand localized infrastructure management options even as cloud adoption grows. Hybrid deployment models that blend cloud and on-premise capabilities are becoming the preferred approach for these sectors.

Expanding DevOps Ecosystem and Sub-Market Potential

Growth extends beyond the core automation tools space. Related markets within the DevOps ecosystem are also scaling at a significant pace as organizations invest in broader transformation initiatives.

- The broader development-to-operations market is projected to be $38.43 billion by 2030. This figure captures the full scope of DevOps transformation across organizational processes, culture shifts, and platform investments that extend beyond individual automation tools into areas such as team structure, release management, and operational governance.

Conclusion

The DevOps automation tools market has moved well beyond its early adoption phase and is now a central pillar of enterprise IT strategy. From 2025 to 2026, confirm strong growth in market valuation, high levels of enterprise adoption, and consistent regional expansion across North America, Asia Pacific, and Europe.

With projected valuations exceeding $72 billion by 2032 and rising investment in AI-driven operations, infrastructure-as-code, and deployment automation, the market trajectory is clear. Organizations that invest early in scalable DevOps automation services stand to gain measurable advantages in delivery speed, operational resilience, and long-term cost efficiency.