Enterprise AI adoption has shifted from experimentation to operational reality across major functions. As models become more accessible through cloud platforms and packaged tools, enterprises are funding production use cases that touch customer experience, risk, finance, engineering, and operations.

Enterprise AI adoption statistics help quantify that shift through market sizing, deployment patterns, and regional momentum. They also surface where enterprise programs concentrate spending, which technologies get prioritized first, and what growth signals to watch as adoption scales across industries.

What Is Enterprise AI Adoption?

Enterprise AI adoption is the process of implementing artificial intelligence across an organization’s workflows, systems, and teams. It includes selecting models, building data pipelines, integrating outputs into applications, and setting governance that keeps performance, security, and compliance aligned with business needs.

It matters because AI outcomes depend on execution, not just capability. Strong adoption connects AI to measurable workflows, makes results repeatable across departments, and reduces the risk of isolated pilots that never reach production.

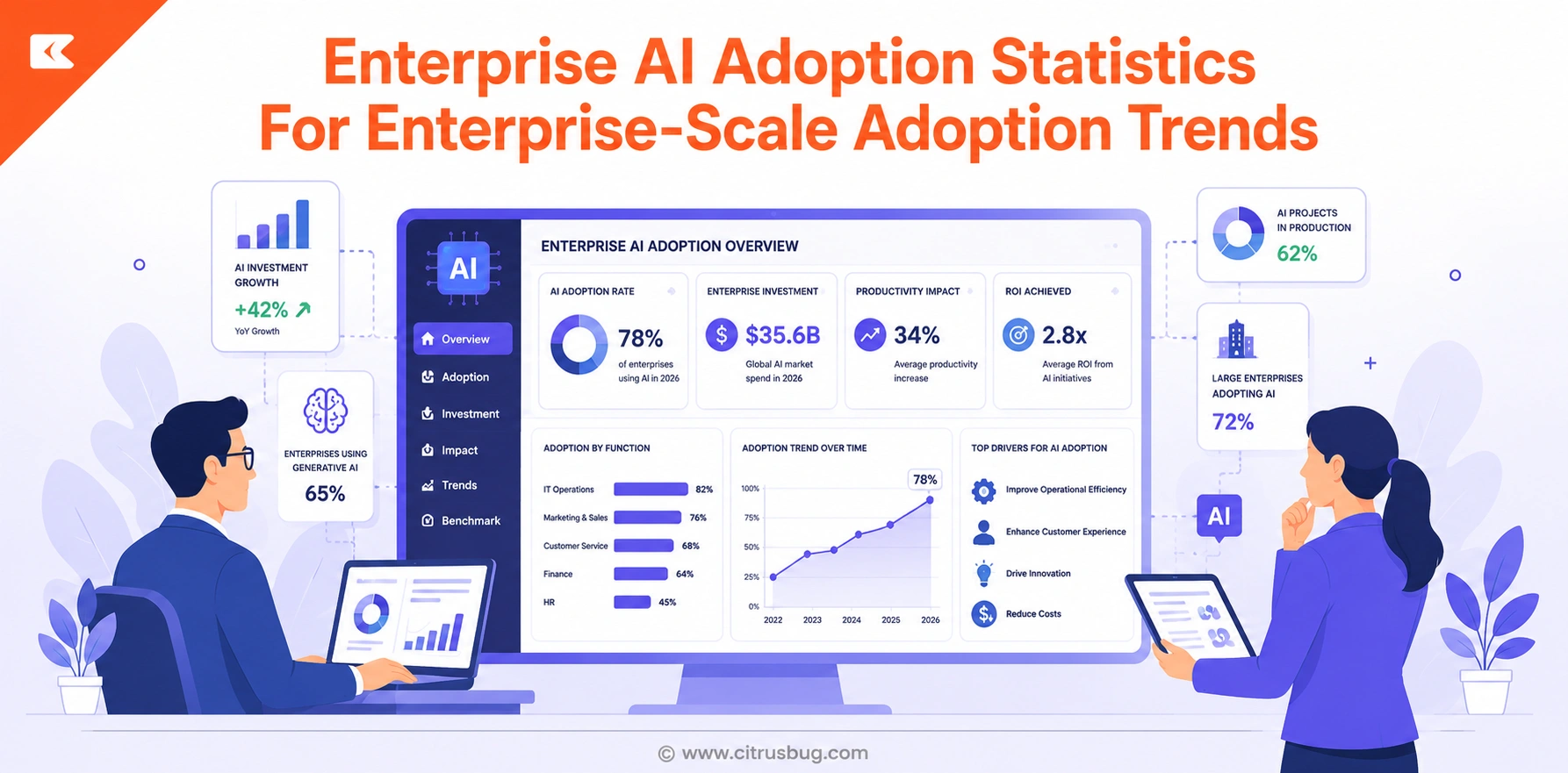

Enterprise AI Adoption Statistics Market Overview

Enterprise AI adoption is expanding because enterprises keep shifting decision-making and automation into software. Adoption accelerates when AI becomes easier to deploy, easier to govern, and easier to scale across teams without heavy infrastructure buildout.

The market signals below show how quickly enterprise AI is growing, alongside the broader AI economy that fuels budgets, talent, and platform maturity.

Enterprise AI Market Scale

Current enterprise AI sizing offers a clear view of how quickly AI is moving into standard enterprise spending. Market expansion here often follows cloud readiness, data platform maturity, and strong demand for automation.

- The enterprise AI market was valued at USD 23.95 billion in 2024, reflecting active production deployments beyond pilots.

- The enterprise AI market was expected to reach USD 31,512.9 million in 2025, showing continued enterprise investment momentum.

Growth Rate Signals

Growth rates matter because they indicate how fast adoption becomes normal across departments, not just within innovation teams. High growth periods usually correlate with faster rollout templates, stronger tooling, and more predictable governance patterns.

- Enterprise AI was forecast to expand at a CAGR of 37.6% from 2025 to 2030, signaling sustained scaling pressure across enterprise stacks.

Broader AI Spend Tailwinds

Enterprise AI programs do not grow in isolation. Broader AI market growth increases vendor competition, expands tool ecosystems, and improves model availability across cloud and software platforms.

- The global AI market was valued at USD 294.16 billion in 2025, indicating a large baseline of commercial AI investment.

- The market is projected to grow to USD 375.93 billion in 2026, which aligns with expanding enterprise AI budgets.

Adoption And Usage Statistics Across Enterprise Programs

Adoption becomes durable when AI is deployed in a way that teams can repeat, govern, and maintain. Enterprise programs typically scale through cloud deployment, concentrated adoption in large organizations, and heavy use of language-driven workflows.

The usage signals below highlight how enterprises deploy AI, where demand concentrates, and which technology patterns show up early in production.

Cloud-Led Enterprise Deployments

Cloud deployment tends to dominate when enterprises need faster rollout cycles and elastic compute. It also supports shared model access across teams that build, test, and monitor AI systems.

- Cloud deployment accounted for around 62.9% of revenue in 2024, reinforcing cloud as the most common rollout model.

Large Enterprise Concentration

Large enterprises usually lead adoption because they have larger data footprints, stronger budgets, and clearer governance teams. They also tend to fund platform-wide AI centers of excellence that support multiple business units.

- Large enterprises held the largest revenue share of around 64% in 2024, signaling strong concentration of adoption in enterprise-scale organizations.

Language-Driven Workloads In Production

Language-driven workflows tend to scale quickly because they map to enterprise content, support, and knowledge systems. These workloads often show up first as assistants, summarization, search, and analytics inside existing tools.

- Natural language processing held a revenue share of over 33.40% in 2024, reflecting wide usage across enterprise communication and document-heavy workflows.

(Source: Precedenceresearch)

Segmentation Insights Across Enterprise Adoption Pathways

Enterprise AI adoption rarely scales evenly. It expands through specific segments first, then spreads as playbooks become repeatable. Market-based segmentation helps explain where adoption consolidates, how deployment decisions evolve, and which verticals absorb AI fastest.

The segmentation signals below reflect where enterprise AI programs concentrate effort as they move from early adoption to broader operationalization.

End-Use Concentration In IT And Telecom

Digital-first industries tend to adopt AI earlier because they operate large volumes of data and automate customer interactions at scale. These verticals also fund AI infrastructure, security controls, and production monitoring sooner.

Early Vertical Spend Signals

The IT and telecom segment captured USD 2.98 billion in revenue share in 2024, showing how strongly this vertical contributes to enterprise AI activity.

Long-Run Expansion Expectations

The same segment was projected to grow at a CAGR of 32.40% from 2025 to 2034, reflecting continued demand for enterprise AI across core digital infrastructure environments.

On-Premises Persistence For Sensitive Workloads

Cloud dominates many deployments, but on-premises remains relevant where data sensitivity and operational control drive architecture decisions. Adoption in this segment often focuses on regulated or proprietary data environments.

Growth Signal For Controlled Deployments

On-premises deployment was expected to expand at a CAGR of 31.80% over the projection period, indicating ongoing investment in controlled infrastructure choices.

SME Acceleration As Tooling Matures

SME adoption expands when AI tooling becomes easier to configure and cheaper to run. Packaged platforms and managed services tend to reduce the barrier to entry, especially for workflow automation and customer engagement use cases.

Fast-Growth Signal In Smaller Organizations

Small and medium enterprises were predicted to experience the quickest CAGR of 38.6% over the projection period, indicating rapid expansion beyond large enterprises.

(Source: Precedenceresearch)

Factors Accelerating Market Growth

Enterprise AI adoption speeds up when three conditions improve at the same time: budgets rise, tooling becomes easier to scale, and organizations build confidence in production governance. These factors reduce the operational friction that slows AI programs after pilot phases.

The growth signals below show how spending and market expansion support broader enterprise adoption in practical terms.

Rising Enterprise Spend On Generative AI

Generative AI budgets often act as a leading indicator because they fund assistants, automation, and knowledge workflows that scale across teams. Increased spending also funds governance, evaluation, and security hardening.

- Enterprise spending on generative AI reached USD 13.8 billion in 2024, indicating strong budget allocation toward production-grade genAI use cases.

Expanding Enterprise Generative AI Market Values

Market expansion reflects broader vendor ecosystems, more enterprise tooling, and stronger platform maturity. These conditions typically reduce implementation overhead for enterprise teams.

- The enterprise generative AI market was estimated at USD 5,245.12 million in 2026, reflecting continued scaling across enterprise environments.

Scaling Enterprise AI In The Core Market

Enterprise AI spending increases as organizations standardize model operations, data controls, and system integration patterns. When adoption becomes repeatable, more departments move from pilots to ongoing usage.

- The enterprise AI market size stood at USD 114.87 billion in 2026, highlighting substantial enterprise investment in scalable AI deployments.

Key Trends And Emerging Patterns

Enterprise AI adoption is being shaped by several powerful forces that are redefining how organizations build, deploy, and scale AI programs.

Understanding these trends helps enterprises prioritize investments, anticipate shifts in the competitive landscape, and position AI as a core operational capability rather than a tactical add-on.

Agentic AI And Autonomous Workflow Automation

- Enterprises are moving beyond simple chatbots toward autonomous AI agents capable of executing multi-step tasks across systems without constant human intervention.

- Agentic AI is being deployed in procurement, customer onboarding, IT operations, and compliance workflows where speed and consistency matter more than human involvement at every step.

- Multi-agent frameworks allow enterprises to chain specialized AI models together, enabling complex processes that no single model could handle alone.

- AI agents are increasingly integrated with enterprise tools such as ERP systems, CRM platforms, and cloud storage to complete real workflows rather than simulate them.

- Governance and human oversight layers are becoming a standard part of agentic deployments to manage risk and ensure agents operate within defined boundaries.

- The shift toward agentic AI is reducing the need for manual task coordination and enabling faster cycle times across high-volume back-office operations.

AI Governance, Risk, And Compliance Standardization

- Enterprises are building formal AI governance structures that include model registries, audit trails, explainability requirements, and bias monitoring as part of standard deployment practice.

- Growing regulatory pressure from frameworks such as the EU AI Act is pushing organizations to treat AI compliance as a mandatory operating requirement rather than a discretionary effort.

- Chief AI Officers and AI ethics boards are becoming more common in large enterprises as leadership accountability for AI decisions moves up the organizational hierarchy.

- Data lineage and consent management are becoming closely tied to AI governance, especially in industries like healthcare, finance, and insurance where regulatory scrutiny is high.

- Standardized governance frameworks are helping enterprises accelerate responsible AI deployment by reducing the uncertainty that previously slowed enterprise-wide rollouts.

Retrieval-Augmented Generation In Enterprise Knowledge Systems

- Retrieval-augmented generation (RAG) is becoming the preferred architecture for enterprise AI applications that need to answer questions based on proprietary, up-to-date, or domain-specific knowledge.

- Enterprises are connecting RAG pipelines to internal knowledge bases, documentation systems, product catalogs, and customer records to give AI models access to accurate, current information.

- RAG reduces the risk of hallucination in high-stakes enterprise contexts by grounding model outputs in verified source documents rather than relying solely on trained parameters.

- Industries such as legal, healthcare, financial services, and manufacturing are adopting RAG-based assistants to surface complex technical information quickly and accurately.

- Multimodal RAG extensions are emerging that allow enterprises to query across text, tables, charts, and images simultaneously, expanding use cases into visual and structured data domains.

AI-Driven Personalization At Enterprise Scale

- Real-time personalization engines powered by machine learning are being embedded directly into customer-facing applications, enabling dynamic content, pricing, and service routing decisions.

- AI personalization is moving beyond consumer products into B2B contexts, where it is used to tailor sales outreach, account management communications, and partner enablement programs.

- Employee experience platforms are incorporating AI-driven personalization to surface relevant training content, automate workflow suggestions, and reduce cognitive load for knowledge workers.

- Privacy-preserving personalization techniques such as federated learning and on-device inference are gaining traction as enterprises balance personalization with data sovereignty obligations.

- Enterprises that have deployed AI personalization at scale are reporting measurable improvements in customer retention, engagement rates, and employee productivity metrics.

Edge AI And Distributed Intelligence In Operations

- Edge AI is gaining significant traction in manufacturing, logistics, retail, and energy sectors where real-time decision-making at the point of data collection is critical to operational efficiency.

- Predictive maintenance, quality inspection, and inventory monitoring are among the leading operational use cases being enabled through edge AI deployments in asset-intensive industries.

- The convergence of edge computing hardware improvements and more efficient small language models is making it practical to run sophisticated inference tasks on low-power devices at the network edge.

- Enterprises are building hybrid architectures that combine edge inference for speed-sensitive tasks with cloud processing for model training, aggregation, and oversight functions.

- Edge AI is enabling new automation capabilities in field operations, remote asset monitoring, and distributed retail environments where centralized cloud processing introduces unacceptable delays.

Regional Market Share And Growth Insights

Enterprise AI adoption patterns vary by region because AI readiness, investment ecosystems, and industry mix differ. Regional signals help identify where adoption is most mature, where growth is fastest, and where enterprises are scaling AI into production.

North America

- North America held a 36.9% share in 2024, reflecting a strong concentration of enterprise AI investment and production deployments.

Middle East And Africa

- The region generated USD 2,368.1 million in enterprise AI revenue in 2024, supported by infrastructure and platform expansion. The regional growth rate was expected to be 38.3% from 2025 to 2030.

Japan

- Japan generated USD 1,408.5 million in enterprise AI revenue in 2024, reflecting growing enterprise adoption across major industries. The market was expected to grow at a 36.7% CAGR from 2025 to 2030.

Future Outlook And Opportunities

- Enterprise AI adoption will shift from project-based initiatives to fully integrated, enterprise-wide platforms that support multiple models, teams, and continuous use cases across every business function.

- Generative AI will expand from content and language tasks into decision-support, financial modeling, supply chain planning, and clinical decision-making as model reliability and governance frameworks improve.

- AI agents and autonomous workflows will become standard in back-office operations, reducing manual effort in areas such as procurement, compliance reporting, HR administration, and customer service escalations.

- Small and mid-sized enterprises will accelerate AI adoption as managed AI services, low-code platforms, and pre-built vertical solutions lower the entry barrier and reduce the need for in-house AI expertise.

- Edge AI deployments will proliferate in manufacturing, logistics, retail, and healthcare settings, enabling real-time intelligence at the point of action without dependence on centralized cloud infrastructure.

- AI governance will evolve into a formal enterprise discipline with dedicated teams, regulatory compliance workflows, model audit infrastructure, and board-level accountability for AI risk management.

- The convergence of AI with other transformative technologies such as quantum computing, digital twins, and the Internet of Things will create new categories of enterprise intelligence that do not yet have established market definitions.

Conclusion

Enterprise AI is moving toward standardized, production-first programs, backed by clear market growth and heavy cloud deployment momentum. Regional signals also show that adoption is expanding across both mature and emerging markets.

Enterprise AI adoption statistics help frame where budgets concentrate, what deployment models dominate, and how adoption may scale across the next decade of enterprise software.