Revenue cycle management statistics have become a critical reference point for healthcare leaders navigating a complex and increasingly pressured financial environment. Across hospitals, physician groups, and payer organizations, the ability to manage billing, claims, and reimbursement with speed and precision has shifted from a back-office function to a strategic organizational priority.

As healthcare systems contend with growing patient volumes, escalating payer complexity, and tighter operating margins, the financial performance of revenue cycle operations directly determines sustainability. Automated platforms, AI-driven tools, and managed outsourcing models are reshaping how providers capture, protect, and optimize revenue.

The numbers tell a compelling story. From double-digit market growth to accelerating AI adoption, the data reveal a sector at the center of healthcare’s digital transformation and operational future.

Key Revenue Cycle Management Statistics at a Glance

| Statistic | Value |

| Global RCM market size (2025) | $86.45 billion |

| Projected market size (2026) | $95.22 billion |

| AI adoption in RCM | 63% (healthcare organizations) |

| AI used for clinical documentation & coding | 48% |

| Services segment share | 67.7% |

| North America’s global market share | 49.73% |

| Software segment share (2026) | 79.65% |

| Claims & denial management share | 34.2% |

| Cloud/SaaS share in U.S. RCM market | 47.90% |

What is Revenue Cycle Management?

Revenue cycle management (RCM) is the financial process that connects clinical care delivery to payment collection within healthcare organizations. It covers every step from patient registration and insurance verification through medical coding, claims submission, denial management, and final payment reconciliation.

Effective RCM ensures that healthcare providers receive accurate and timely reimbursement for services rendered. As billing complexity deepens alongside changing payer requirements and value-based care models, RCM systems help organizations reduce claim errors, minimize denials, and protect the cash flow that keeps operations running.

Revenue Cycle Management Statistics: A Market Overview

Healthcare’s financial infrastructure is expanding at a scale that reflects growing institutional commitment to billing accuracy, claims automation, and reimbursement efficiency. Increased patient volumes, rising coding complexity, and the transition toward value-based care are compressing margins in ways that make RCM investment a necessity rather than a discretionary decision.

Global Market Size and Momentum

The global RCM market is expanding across software, services, and outsourcing segments, reflecting broad institutional investment in healthcare financial management across all care settings and geographies.

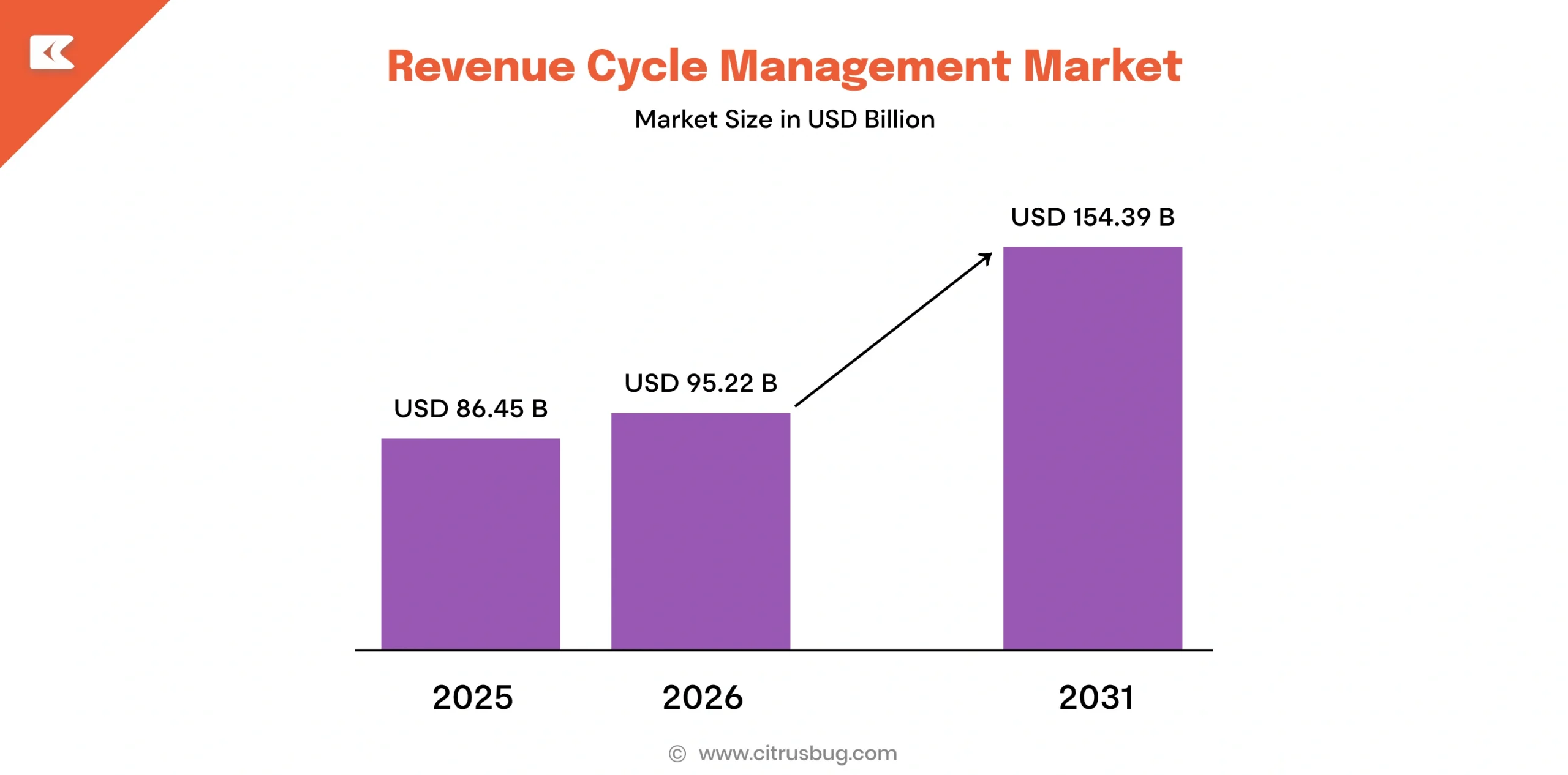

- The global revenue cycle management market reached $86.45 billion in 2025, with increasing demand for automated healthcare billing and financial workflow solutions across hospital systems and payer organizations worldwide.

- Market size is expected to grow to $95.22 billion in 2026, advancing at a compound annual growth rate (CAGR) of 10.15% through 2031 as AI adoption and outsourcing accelerate across all care settings.

RCM Product Solutions and Outsourcing Scale

The market’s scope extends from standalone billing software to full managed service outsourcing, with each segment growing independently as healthcare organizations adopt strategies aligned with their size, complexity, and administrative capacity.

- The revenue cycle management product solutions market, covering software platforms and billing tools, was valued at $58.27 billion in 2024, projected to grow at a CAGR of 12.4% through 2030 as providers shift from legacy billing systems to integrated digital platforms.

- The global healthcare RCM outsourcing market stood at $23.47 billion in 2025, reflecting health systems’ growing preference for delegating billing, coding, and denial management to specialized third-party vendors.

The Services Segment Commanding the Largest Share

Among the core RCM market segments, services including managed billing and outsourced revenue cycle operations consistently lead in revenue share. This reflects a structural preference across healthcare for delegating complex financial functions rather than managing them entirely in-house.

- The services segment held 67.7% of the global revenue cycle management market in 2025, driven by the growing trend of outsourcing RCM functions to specialized providers as clinical and administrative complexity increases.

How Healthcare Organizations Are Adopting RCM Tools

Revenue cycle management statistics on technology adoption reveal a sector making decisive choices about automation, cloud platforms, and managed billing operations. Healthcare providers across all settings are integrating digital tools at a pace that outpaces most other health technology investment categories.

AI Automation Taking Hold Across Revenue Cycle Operations

AI integration is changing the foundational logic of healthcare billing. Instead of manual reviews and reactive claim responses, organizations are building predictive and automated workflows that handle billing volume at scale without equivalent increases in staffing.

- 63% of healthcare organizations have already integrated AI-powered automation solutions into their revenue cycle in 2024, with claims processing, denial management, and revenue integrity as the most common application areas.

- 48% of healthcare organizations specifically apply AI to clinical documentation and medical coding within the revenue cycle, reflecting a structural shift toward intelligent automation in the most labor-intensive billing processes.

Cloud and Web-Based Deployment Leading Adoption Choices

Provider organizations across regions are selecting cloud-based and browser-accessible platforms over on-premise installations. Lower infrastructure costs, remote accessibility, and real-time EHR integration are the primary factors behind this deployment preference.

- Web-based delivery mode represented 51.20% of the global RCM market revenue in 2025, reflecting provider preference for browser-accessible platforms that connect directly with electronic health records and enable real-time claims visibility without heavy IT infrastructure.

- In the U.S. specifically, the RCM services segment held 53.60% of the 2024 market share, as healthcare providers moved toward managed billing operations and end-to-end outsourced revenue cycle functions rather than purely in-house models.

Key Trends Shaping the Revenue Cycle Management Market

Revenue cycle management statistics from leading healthcare surveys and market studies confirm that the industry is undergoing structural change rather than gradual evolution. Several clear patterns have emerged across providers, payers, and technology vendors that are redefining how revenue cycle operations are built, managed, and measured.

AI Investments Generating Measurable Financial Returns

The conversation around AI in RCM has moved decisively from potential to performance. A growing share of organizations have moved past early adoption and are now reporting tangible returns from automation investment.

- 42% of healthcare RCM leaders expect high ROI from automation investments over a five-year horizon, signaling strong industry confidence in AI-driven billing transformation as a long-term strategic priority beyond cost containment.

- 15% of healthcare organizations have already achieved positive ROI from AI-powered RCM automation solutions, demonstrating that intelligent billing automation delivers real financial benefits including reduced denials, faster reimbursements, and lower administrative costs.

Outsourcing Transitioning from Option to Operational Standard

Medical practices and health systems are increasingly choosing to delegate revenue cycle functions rather than build internal capabilities. This shift reflects both the operational complexity of modern billing environments and the growing maturity of specialized RCM vendors that offer depth, scalability, and measurable outcomes.

- 36% of medical practice leaders report their organizations plan to outsource or automate part of their revenue cycle management in 2025, with collections, billing, and medical coding as the most commonly targeted functions for delegation.

Market Growth Confirming Sustained Healthcare Finance Priority

Double-digit growth rates across the RCM market reflect genuine financial pressure on providers to improve billing accuracy and reduce the cost of revenue recovery. The consistent investment signals that healthcare organizations view RCM not as a periodic upgrade but as an ongoing operational priority. Technology vendors are responding with more accessible and scalable platforms designed to serve both large health systems and independent practices across all specialties.

- The revenue cycle management market is advancing at a global CAGR of 12.1%, driven by the combined effect of healthcare digitization, AI-powered billing platforms, and expanding insurance coverage across global markets.

Integrated Platforms Replacing Fragmented Billing Systems

Disconnected point solutions across front-end registration, mid-cycle coding, and back-end collections are giving way to unified platforms that consolidate the entire revenue cycle into a single connected workflow.

Healthcare organizations are prioritizing systems that reduce manual handoffs between departments, eliminate data entry redundancy, and give finance teams unified visibility into claim status and payment performance. As billing complexity rises across payer contracts and coding requirements, fragmented systems create compounding costs that integrated RCM platforms are specifically designed to eliminate.

Revenue Cycle Management Market Share Across Global Regions

Regional adoption and market strength vary significantly, shaped by healthcare infrastructure maturity, payer complexity, the pace of digital health investment, and regulatory environments. North America, Europe, Asia Pacific, and the United States each present distinct RCM market characteristics that reflect their healthcare delivery models and administrative infrastructure.

North America

- North America holds the dominant position in the global RCM market, commanding 49.73% of global market share in 2025. The region’s complex multi-payer insurance environment, high healthcare expenditure, and strong AI and cloud adoption by hospital networks make it the largest and most mature RCM ecosystem worldwide.

United States

- The U.S. healthcare revenue cycle management market is projected to reach $72.97 billion in 2026, fueled by rising healthcare investments, chronic disease prevalence, and expanding Medicare and Medicaid enrollment that creates increasingly complex billing and reimbursement requirements for providers at every care setting.

Europe

- Europe’s revenue cycle management market reached $10.57 billion in 2024, with adoption driven by healthcare providers’ focus on financial efficiency and optimized billing workflows. Fragmented national billing codes across EU member states and GDPR data localization requirements add implementation complexity but simultaneously drive demand for standardized RCM platforms across the region.

Asia Pacific

- Asia Pacific is the fastest-growing RCM region globally, with healthcare digitization accelerating across India, Singapore, and Australia. Over 600 hospitals in India have fully digitized their billing and claims management systems in 2025, replacing manual processes with automated RCM platforms to improve coding accuracy, financial transparency, and reimbursement speed.

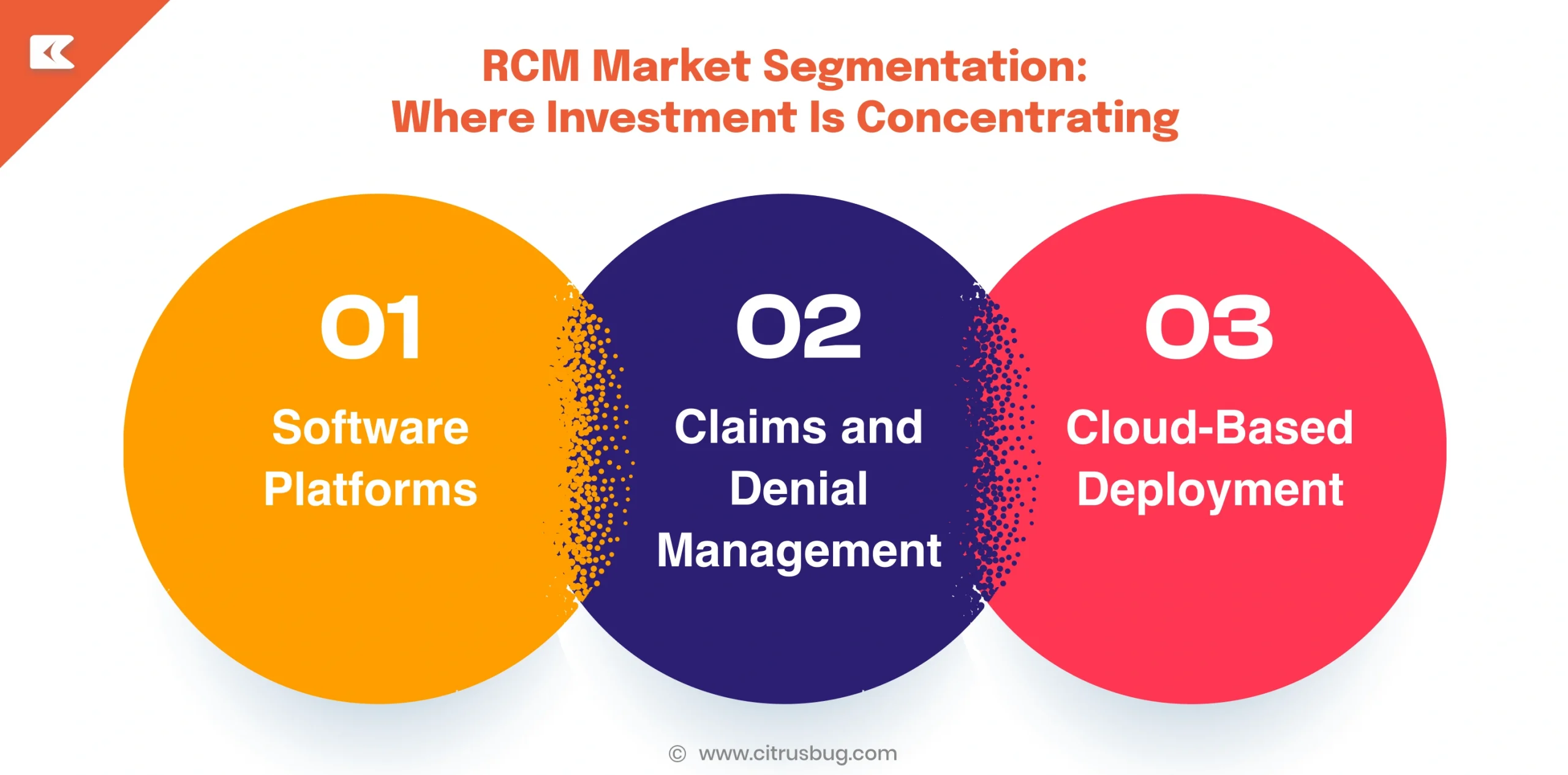

RCM Market Segmentation: Where Investment Is Concentrating

Revenue cycle management statistics broken down by product type, deployment model, and application area reveal a market with clear investment priorities. Healthcare organizations are not investing broadly across all RCM categories equally; specific segments are capturing disproportionate attention and budget. Software platforms, claims management tools, and cloud-based delivery models have emerged as the most consistently prioritized investment areas across provider types and geographies.

Software Platforms

The transition from paper-based and legacy billing systems to purpose-built software platforms has accelerated significantly over the past three years. Healthcare organizations of all sizes are standardizing on integrated software that connects clinical documentation with billing workflows and payer communication.

The software segment is projected to hold 79.65% of the total RCM market share in 2026, driven by advanced integrated platforms that enable unified workflows using AI in medical billing, coding, denial management, and EHR connectivity. As cloud adoption expands and AI becomes embedded directly into billing engines, software’s market dominance reflects a structural shift away from services-only models.

Claims and Denial Management

Claims and denial management remains the highest-value and most resource-intensive function in the revenue cycle. The financial impact of denied and delayed claims is substantial, and the volume of denials has grown in complexity as payer rules evolve and documentation requirements tighten.

In the U.S. RCM market, claims and denial management accounted for 34.2% of market share in 2024, representing the largest functional application segment. Providers are directing significant investment toward denial prevention strategies, automated eligibility verification tools, and real-time claim scrubbing technologies to reduce the financial impact of rejected reimbursements before they occur.

Cloud-Based Deployment

Cloud-based delivery has become the default choice for healthcare organizations evaluating new RCM platforms. The ability to scale without capital hardware investment, support geographically distributed teams, and integrate continuously with health information systems makes cloud platforms the most practical deployment option across provider types.

In the 2024 U.S. revenue cycle management market, cloud-based and SaaS platforms held a 47.90% market share, reflecting rapid provider migration to scalable digital billing platforms. This deployment mode continues to grow as organizations prioritize remote access, faster software updates, and direct integration with EHRs without on-premise IT overhead. Cloud platforms also reduce implementation timelines significantly, allowing organizations to move from contract to a fully operational billing workflow in weeks rather than months.

Why Healthcare Organizations Continue to Invest in RCM

Several interconnected forces are driving sustained investment and adoption across the global RCM market. These factors reflect both structural changes in healthcare delivery and operational realities that are pushing organizations to modernize their financial infrastructure.

Rising Patient Volumes and Chronic Disease Burden

As populations age and chronic conditions like diabetes, heart disease, and respiratory illness become more prevalent, healthcare utilization is rising steadily. Higher patient volumes mean more billing events, more claims, and greater administrative complexity across every care setting, all of which increase the operational demand placed on revenue cycle infrastructure and the teams that manage it.

Transition to Value-Based Care Reimbursement

The shift from fee-for-service to value-based payment models requires healthcare providers to track outcomes, quality metrics, and cost data alongside traditional billing. This added layer of reporting complexity creates strong demand for RCM platforms that can manage both transactional billing and performance-based contract compliance simultaneously, within a single integrated workflow.

EHR Integration and Interoperability Requirements

Government requirements around electronic health records and interoperability are pushing healthcare organizations to digitize their administrative workflows at an accelerating pace. As EHR systems become standard across care settings, the need for RCM platforms that connect directly with clinical documentation has driven deployment of integrated billing solutions across hospitals, clinics, and specialty practices.

Growing Administrative Complexity Across Payer Contracts

Multi-payer environments combining Medicare, Medicaid, commercial insurance, and self-pay create billing requirements that vary significantly by contract. Each payer maintains different coding rules, claim formats, prior authorization thresholds, and denial criteria. The resulting administrative burden makes automated RCM tools a practical necessity for organizations managing billing at any meaningful volume.

AI and Automation Technology Maturation

AI-powered billing tools have moved from experimental use cases to production-grade deployments across the revenue cycle. Advances in natural language processing for clinical documentation, machine learning models for denial prediction, and automation for claims submission have made AI-enabled RCM both more reliable and cost-effective than earlier iterations, lowering the barrier to adoption for mid-sized and smaller provider organizations.

Revenue Cycle Management Market Projections Through 2032

The global revenue cycle management market is on a clear long-term growth trajectory supported by AI investment, outsourcing acceleration, and expanding healthcare coverage across emerging regions. Each segment, from software platforms to back-end operations, is tracking toward substantial scale by 2030 and 2032.

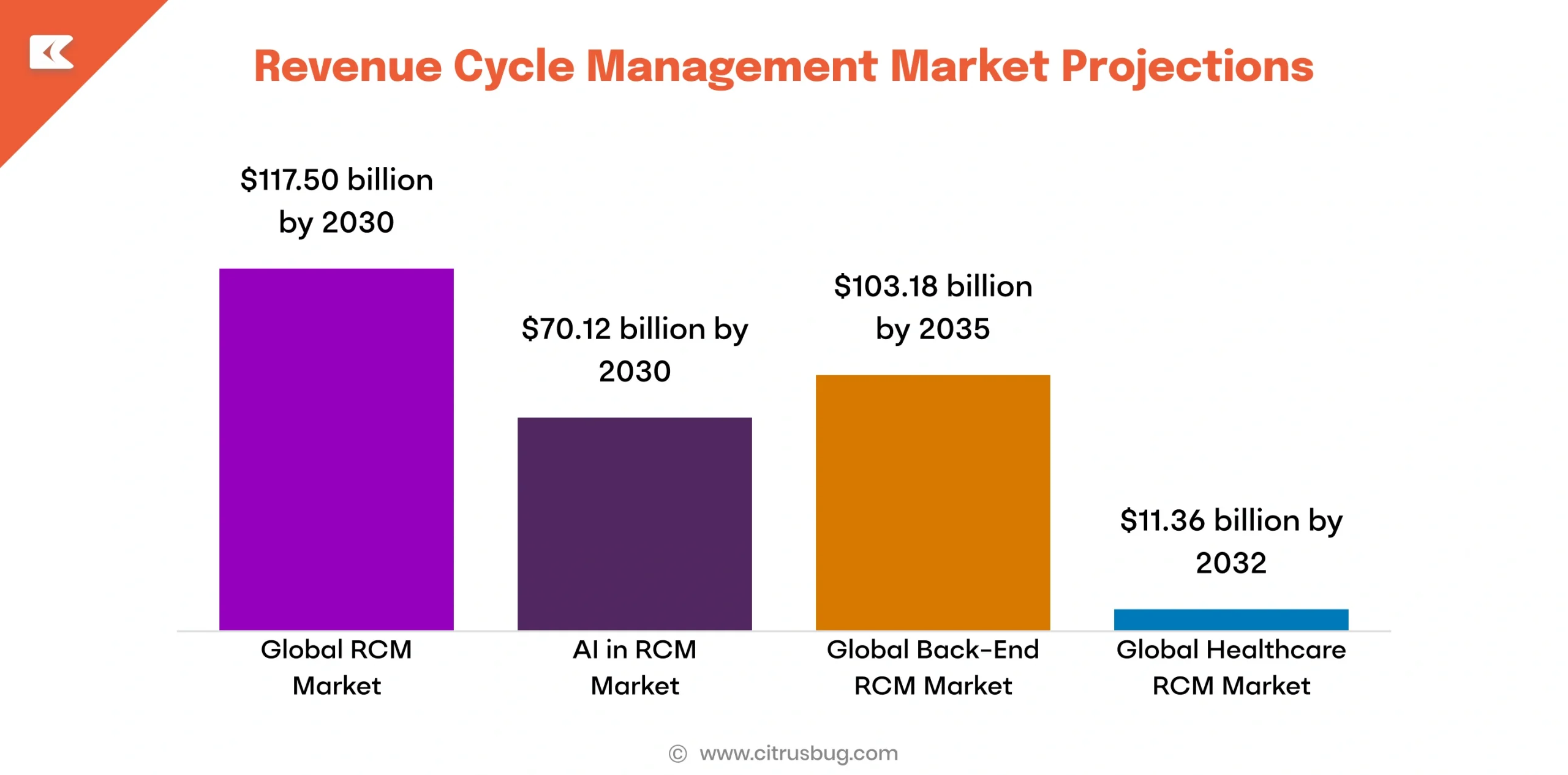

- The global revenue cycle management product solutions market is projected to reach $117.50 billion by 2030, representing a major expansion opportunity as AI-driven billing automation and value-based care continue to transform healthcare financial operations across all provider categories.

- The AI in revenue cycle management market specifically is projected to reach $70.12 billion by 2030, growing at a CAGR of 24.16% from 2025, with North America accounting for more than 55% of total revenue as predictive analytics and automation redefine claims management at scale.

- The global back-end revenue cycle management market is projected to grow from 38.57 USD Billion in 2025 to 103.18 USD Billion by 2035, exhibiting a compound annual growth rate (CAGR) of 10.34% during the forecast period 2025 – 2035.

- The global healthcare RCM outsourcing market is expected to reach $11.36 billion by 2032, advancing at a CAGR of 15.2%, making it the fastest-growing individual segment in the RCM ecosystem, as healthcare organizations accelerate cost-containment through outsourced front-end, mid-cycle, and back-end billing operations.

Conclusion

Revenue cycle management statistics make it clear that healthcare’s financial infrastructure is at a defining inflection point. From double-digit market growth and accelerating AI adoption to clear ROI signals and expanding regional investment, the numbers reflect an industry making serious, sustained commitments to operational transformation in billing and revenue management.

For healthcare organizations still relying on fragmented billing workflows or manual claims processes, the data presents a compelling case for action. Purpose-built revenue cycle management services can help providers build resilient RCM software to reduce denials, accelerate reimbursement cycles, and build a more financially resilient operation suited to the demands of modern healthcare delivery.